2026 Tax Brackets Are Bigger, Deductions Are Higher. Here’s What That Actually Means for Your Paycheck

The IRS has officially updated the federal income tax brackets and standard deductions for 2026, and the changes matter more than most people realize. Not because tax rates changed (they didn’t), but because the brackets widened and deductions increased, which affects how much of your income gets taxed at each rate.

In plain terms: many taxpayers will keep a little more of their income in 2026 compared with 2025, even if their salary goes up slightly.

Below is what changed, why it matters, and what smart tax planning looks like going into 2026.

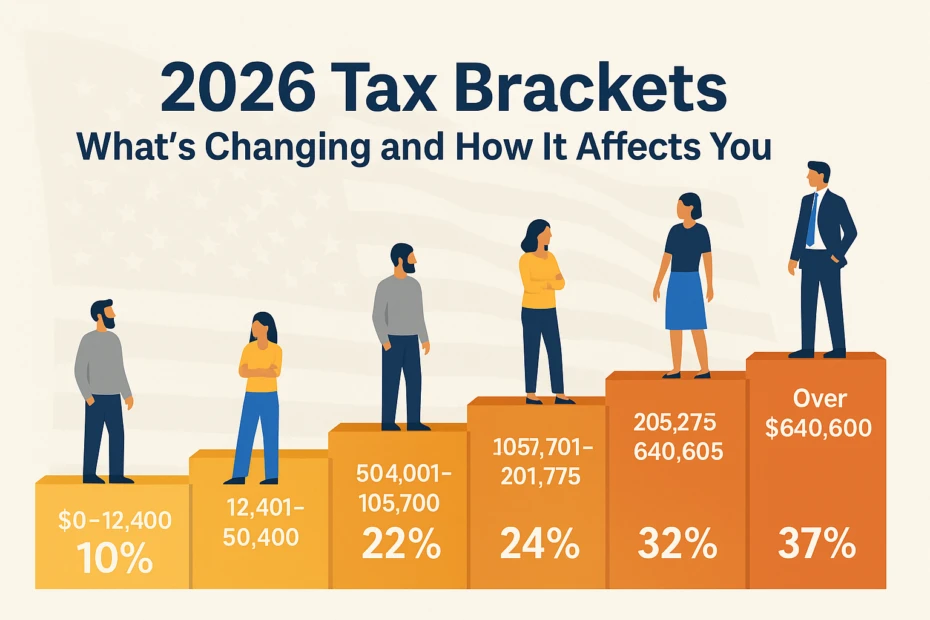

1) The IRS kept the same seven tax brackets (but adjusted the income ranges)

For 2026, the IRS maintained the same seven federal income tax rates: 10%, 12%, 22%, 24%, 32%, 35%, and 37%.

What changed is where those brackets start and end. This happens most years because the IRS adjusts brackets for inflation.

Why this matters

If your income rises, but the brackets also rise, you may avoid being pushed into a higher bracket as quickly. This is one of the main ways inflation adjustments help prevent “silent” tax increases.

2) The standard deduction is higher in 2026

The standard deduction reduces your taxable income before tax brackets even apply. For 2026, the updated standard deduction amounts are:

- Married filing jointly: $32,200

- Single: $16,100

- Head of household: $24,150

Why the standard deduction matters more than people think

For most households, the standard deduction is the biggest and most reliable tax break they’ll get. It reduces taxable income automatically, without needing itemized deductions.

Example: A married couple earning $150,000 does not start paying tax on $150,000. They start paying tax after subtracting the standard deduction, which means the taxable income is much lower.

3) The 12% bracket now stretches further (especially for married couples)

One of the biggest practical takeaways: the 12% bracket for married couples now extends to just over $100,000 of taxable income.

That’s meaningful because it creates more “low-tax space” for:

- Roth conversions

- capital gains planning

- retirees managing withdrawals

- families trying to avoid jumping into the 22% bracket

4) Most people misunderstand marginal tax rates vs effective tax rates

This is where tax anxiety usually gets out of control.

A couple might be told they’re “in the 22% bracket,” and immediately assume they pay 22% on everything they earn. That’s not how the U.S. tax system works.

Marginal tax rate

The marginal tax rate is the rate paid on the last dollar earned (the “top slice” of income).

Effective tax rate

The effective tax rate is the average tax rate paid across total income.

That’s why a household earning $150,000 can have a marginal rate of 22% while still paying an effective rate closer to 10% overall, because large portions of income are taxed at 10% and 12%, and deductions reduce taxable income first.

5) Seniors get additional deductions in 2026

Tax benefits increase once someone reaches age 65. In 2026:

- Seniors receive an extra standard deduction of $1,650 each (if married)

- Unmarried seniors (not a surviving spouse) can receive $2,500

That means a married couple where both spouses are 65+ may get a meaningful increase in total deductions compared with younger households.

6) The “bonus senior deduction” could be a major retirement tax break

The outline includes a new bonus senior deduction of $6,000 per person, potentially totaling $12,000 for married couples.

It also includes income limits for full eligibility:

- Singles: full amount if modified adjusted gross income is $75,000 or less

- Married filing jointly: full amount if modified adjusted gross income is $150,000 or less

Why this matters

If accurate and applicable, this would create a significant tax planning opportunity for retirees who can manage income below the thresholds through strategies like:

- Roth withdrawals instead of IRA withdrawals

- managing capital gains carefully

- timing Social Security and retirement account distributions

- spreading out large taxable events over multiple years

7) Chained CPI can quietly raise taxes over time (even when brackets rise)

This is the part that rarely gets explained clearly.

What is chained CPI?

Chained CPI is a method of calculating inflation that assumes consumers change their behavior when prices rise (for example, buying chicken instead of steak).

Because it often shows inflation as slightly lower than traditional CPI, it can lead to slower increases in:

- tax bracket thresholds

- standard deduction amounts

Why it matters

When brackets rise more slowly than income growth, people can get pushed into higher tax brackets over time. That’s known as bracket creep, and it can feel like taxes are rising even when the official tax rates stay the same.

8) Several income sources remain tax-free in 2026

Tax planning isn’t only about deductions. It’s also about knowing which income streams are not taxed at all.

Here are several key examples:

1) Gifts

In 2026, individuals can give up to $19,000 per person without triggering gift tax reporting requirements in most cases. Married couples can effectively gift $38,000 per person.

2) Inheritances

Inheritances are generally not taxable at the federal level for the recipient. Large estates may face estate tax, but the exemption is very high (the outline references around $15 million).

3) Roth IRA and Roth 401(k) withdrawals

Qualified Roth withdrawals are tax-free when:

- The account holder is age 59½ or older, and

- The account has been open for at least 5 years

This is one of the biggest reasons Roth accounts are so powerful in retirement tax planning.

9) The smartest 2026 tax strategy isn’t “pay less” it’s “plan longer”

The real advantage of understanding tax brackets is not just saving money this year. It’s controlling taxes across decades.

The strongest long-term tax strategies usually focus on:

- Managing taxable income intentionally (instead of accidentally)

- Using deductions strategically (especially for retirees)

- Keeping flexibility across account types (taxable, IRA/401(k), Roth)

- Reducing future tax spikes from RMDs and Social Security taxation

Bottom line

The 2026 tax updates deliver wider brackets and higher deductions, which can reduce taxes for many households especially seniors. But the long-term story is bigger than one year’s tax table. Inflation adjustments help, but chained CPI can still lead to higher taxes over time through bracket creep.

That’s why the best move is not guessing where taxes are headed. It’s building a plan that keeps options open, keeps income flexible, and prevents retirement from becoming a tax surprise instead of a lifestyle upgrade.

All writings are for educational and entertainment purposes only and does not provide investment or financial advice of any kind.