Can John and Jane Retire Early and Spend $11,000 a Month? Here’s How They Made the Math Work

For many near-retirees, the dream is simple: live comfortably, travel, and enjoy the freedom of retirement without worrying about money—or becoming a financial burden to their kids. John and Jane, a couple in their early 60s, are aiming to do just that. But can they really spend $11,000 a month and still retire early?

In this episode, we unpack their financial strategy and how a few smart moves—including tax planning, timing Social Security, and adjusting spending goals—allowed them to retire years ahead of schedule with confidence.

Their Goal: Financial Freedom Without Fear

John and Jane are both working professionals—he’s 64, she’s 62—and they’re planning to retire at 65 and 63. Their goal? Spend $10,000–$11,000 per month throughout retirement, maintain their lifestyle, and never have to rely on their kids for help.

Their motivation is rooted in personal experience. Both witnessed their parents struggle in retirement and don’t want history to repeat itself. They’re looking for balance: enjoy their savings while ensuring it lasts through their 90s.

Where They Stand Today

- John’s 401(k): $1 million

- Jane’s 401(k): $700,000

- Joint brokerage account: $320,000

- Home: Nearly paid off, with a small remaining mortgage

They’re each saving 10% of their salaries into their 401(k)s with a 3% company match, and their investments are projected to grow at 7.2% until retirement, then 6.5% during retirement. While those are optimistic assumptions, their planner ran stress tests to validate sustainability.

The Social Security Plan

One of the smartest elements of their plan? Social Security timing.

- Jane will collect her benefit of $3,100/month at age 67.

- John will wait until 70 to collect $3,900/month.

This gap strategy creates an income dip early in retirement but pays off with higher guaranteed income later on—especially valuable for the surviving spouse.

What Will They Spend—and Can They Afford It?

John and Jane estimate they’ll spend $120,000 annually, or $10,000/month, in today’s dollars—adjusted for inflation. When their mortgage is paid off in year four of retirement, their housing expenses will drop significantly.

Initially, they’ll draw down from their taxable joint account, benefiting from favorable capital gains treatment. Later, RMDs from their IRAs will increase their taxable income, so tax planning becomes critical.

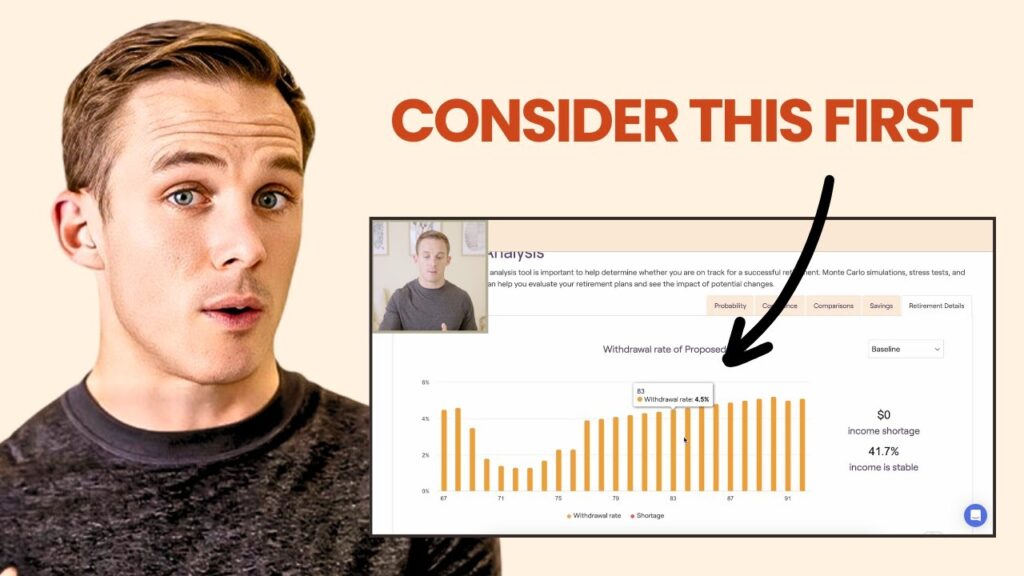

Withdrawal Rate Reality Check

In the early years, their withdrawal rate is projected at 4.5%, which is just slightly above the often-cited “safe withdrawal” threshold of 4%. But as their Social Security income kicks in and their mortgage disappears, that rate drops to just 1.5%. That drop offers a buffer and allows for portfolio growth even as they continue spending.

Can They Spend More? Monte Carlo Has the Answer

Using Monte Carlo simulations, their advisor tested different spending scenarios:

- $10,000/month: 95% probability of success

- $12,000/month: 85% probability

- $14,000/month: 58% probability

So while $14,000/month is doable, it would require tighter management during market downturns. The sweet spot? Retiring earlier but with a modest bump to $11,000/month in spending—which still carries a strong success rate.

The Early Retirement Pivot

John and Jane made a bold decision: retire three years earlier than planned. With fine-tuned planning and updated spending assumptions, they can do it safely. Their new retirement age: 65 and 63, respectively. Their new monthly spending target: $11,000. It’s an inspiring example of how planning can create flexibility, not just constraints.

The Tax Game Plan

In early retirement, they’ll use low-tax years to their advantage:

- Roth conversions while in low tax brackets

- Charitable giving strategies

- Drawing from their joint account first to reduce future RMDs

This thoughtful sequencing reduces lifetime tax liability and gives them greater control over their cash flow.

Insurance and Estate Planning: No Afterthoughts Here

Their strategy also includes:

- Life insurance review

- Long-term care options

- Updated wills and trusts

These aren’t just checkboxes—they’re core to making sure their financial independence remains intact and their legacy is protected.

Social Security: More Than Just a Delay

While John’s plan to delay until 70 maximizes his benefit, they’ve considered the trade-offs. If health issues or market conditions change, they’ve built in flexibility to adapt. It’s not just about maximizing income—it’s about aligning benefits with overall lifestyle and risk preferences.

Bottom Line

John and Jane’s case is a model for modern retirement planning: combining solid savings, strategic withdrawal planning, smart tax moves, and thoughtful lifestyle decisions. With the right plan in place, they’re not just retiring—they’re retiring on their terms.

You should always consult a financial, tax, or legal professional familiar about your unique circumstances before making any financial decisions. This material is intended for educational purposes only. Nothing in this material constitutes a solicitation for the sale or purchase of any securities. Any mentioned rates of return are historical or hypothetical in nature and are not a guarantee of future returns.

Past performance does not guarantee future performance. Future returns may be lower or higher. Investments involve risk. Investment values will fluctuate with market conditions, and security positions, when sold, may be worth less or more than their original cost.