Retirement Planning Case Study: How Michael and Lisa Turned a Risky Future into a Confident Plan

Planning for retirement isn’t just about hitting a “magic number.” It’s about aligning your money with your goals, lifestyle, and timing. Michael and Lisa, both nearing 65, came to the table with a couple million dollars in their portfolio and a dream: to retire comfortably, travel frequently, and maintain the life they’ve built. But when the numbers were put to the test, it became clear that their strategy needed fine-tuning.

Michael and Lisa’s Retirement Goals

With a well-diversified portfolio of joint accounts, 401(k)s, IRAs, Roth IRAs, and nearly $900,000 in home equity, Michael and Lisa looked well-prepared on paper. Their plan was to spend $14,000 per month in retirement about $10,000 on living expenses and $4,000 on travel while waiting until age 70 to collect Social Security.

But here’s the catch: in their first year, they’d need to withdraw about $252,000 from their portfolio, a nearly 10% withdrawal rate. That pace wasn’t sustainable and could have derailed their long-term financial security.

Understanding Cash Flow Needs

A major pitfall in retirement planning is underestimating how cash flow changes year by year. Michael and Lisa’s initial plan didn’t account for the strain of heavy early withdrawals, which could have quickly depleted their savings before Social Security kicked in.

The lesson here? It’s not just about how much you want to spend it’s about how much of that spending your guaranteed income sources (like pensions or Social Security) actually cover.

Strategic Adjustments for Success

With a few targeted changes, Michael and Lisa dramatically improved their outlook:

- Travel for the First 10 Years: Scaling back the $4,000 monthly travel budget after the first decade of retirement reduced long-term spending.

- Portfolio Allocation Shift: Moving from a 60/40 (moderate) to a 70/30 (growth-oriented) portfolio increased their potential returns without adding undue risk.

- Roth Conversions: Shifting pre-tax retirement funds into Roth accounts lowered future tax burdens and gave them more flexibility for withdrawals.

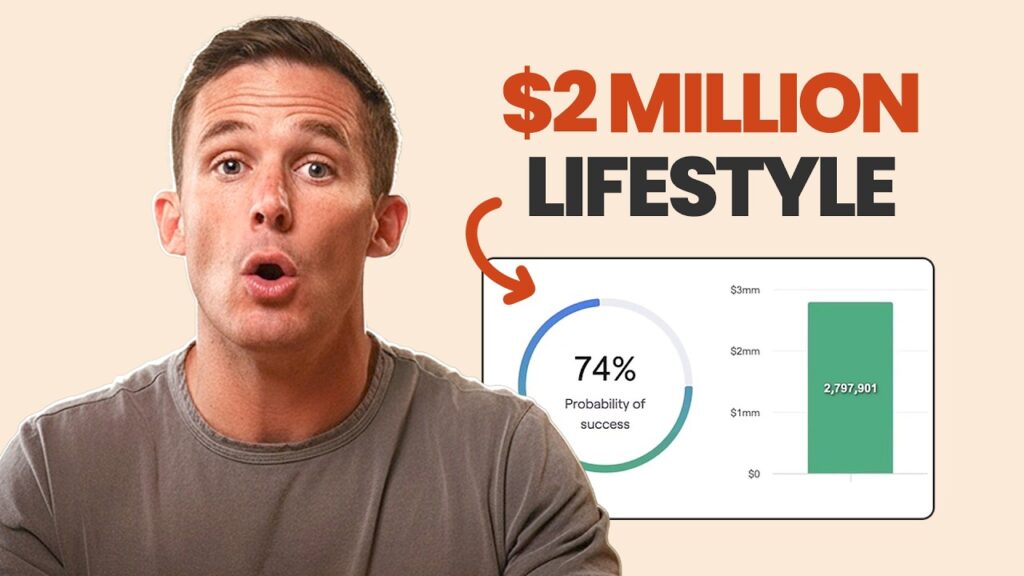

Results of the Adjusted Plan

These changes boosted their probability of success from 32% to 74% a massive improvement that turned their retirement from risky to realistic. Plus, downsizing their home in the future remains an option to add even more flexibility.

Key Takeaways for Your Retirement Plan

Michael and Lisa’s story offers lessons for anyone planning their retirement:

- Model expenses accurately—not just at the start, but across decades.

- Revisit your asset allocation—make sure it matches your goals, not generic rules of thumb.

- Use smart tax strategies—Roth conversions, withdrawal sequencing, and timing Social Security can make a huge difference.

- Build flexibility into your plan—because retirement isn’t a straight line, it’s a journey with shifting needs.

You should always consult a financial, tax, or legal professional familiar about your unique circumstances before making any financial decisions. This material is intended for educational purposes only. Nothing in this material constitutes a solicitation for the sale or purchase of any securities. Any mentioned rates of return are historical or hypothetical in nature and are not a guarantee of future returns.

Past performance does not guarantee future performance. Future returns may be lower or higher. Investments involve risk. Investment values will fluctuate with market conditions, and security positions, when sold, may be worth less or more than their original cost.