What Buyers Should Check Before Completing a Property Purchase

Buying a house does something odd to otherwise sensible people.

You’ve probably spent weeks scrolling through listings, driven past the property three times before booking a viewing, and stood in the kitchen imagining where everything would go. You know which bedroom would be yours, which wall you’d knock through, and roughly what color you’d paint the hallway. What you might not know is when the wiring was last checked, whether the boiler is on its last legs, or whether there’s been water sitting behind the bathroom wall since sometime before you even started looking.

That gap, between how well you know the feel of a house and how little you actually know about its condition, is where expensive surprises live.

The survey your mortgage lender orders is not there to protect you. It exists to protect the bank. It answers one question: is this property worth the money being lent against it? It doesn’t go looking for problems. It doesn’t open anything up or test anything. It doesn’t tell you what the roof timbers look like from the inside or whether the consumer unit should have been replaced a decade ago. If you rely on it as your main due diligence, you’re relying on something that wasn’t designed to do that job.

Exchange of contracts is the moment everything changes. Before that point, you have options. After it, the property and everything in it, every fault, every hidden defect, every slowly failing component, belongs to you. So the time to find things out is before you get there.

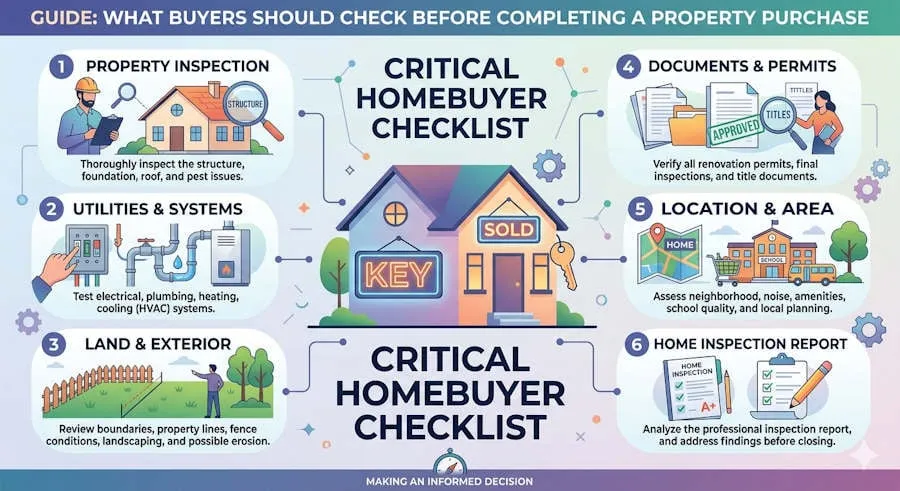

Get a Proper Building Survey Done

The first thing worth understanding is that a mortgage valuation and a building survey are two entirely different documents, and one of the most common mistakes buyers make is treating them as the same thing.

A Level 2 HomeBuyer Report gives you a look at the main visible elements of the property and highlights anything that appears to need attention. A Level 3 Full Structural Survey goes significantly further, into the fabric of the building rather than just its surface, and is worth the extra cost on anything older, anything with obvious signs of wear, or anything that’s been extended or reconfigured at some point in its life.

The difference in cost between the two is typically a few hundred pounds. The difference in what they tell you can be the difference between walking into a purchase with your eyes open and walking into one with a very expensive problem you didn’t know existed until you’d already signed everything.

A thorough survey should cover:

- Structural movement or anything pointing toward settlement and subsidence

- Damp in any form, whether it’s coming in from outside or rising from below

- The state of the roof, the covering, the timbers beneath it, and the condition of flashings and leadwork

- Any repairs that look like they might have been done to conceal something rather than actually fix it

- Extensions or alterations that may never have had the permissions they needed

If the survey turns something up, use it. A significant problem identified before exchange is a legitimate reason to go back to the seller, renegotiate the price, or ask for remedial work to be done before completion. A lot of buyers feel awkward about doing this. It’s worth remembering that the alternative is paying for it yourself, quietly, after you move in.

Electrical Inspection

Think about the house you’re buying and ask yourself honestly: do you know when the electrical installation was last inspected?

Not when a socket was fitted or a light was changed. When a qualified engineer last went through the whole system properly, tested every circuit, checked what was happening inside the walls, and put their findings in writing.

In most cases, the answer is going to be some version of not recently, or nobody thought to ask. Which is how it goes, because there’s nothing visible about an electrical installation that changes appearance as it deteriorates. The cables inside a wall look exactly the same from the outside, whether they’re completely fine or whether the insulation has been quietly breaking down for years. Nothing announces itself. It just gets slowly worse until one day it doesn’t.

Owner-occupied homes should have a full Electrical Installation Condition Report every ten years. Rented properties every five. A lot of properties haven’t had one anywhere near as recently as that, and nobody has done anything about it because nothing has obviously gone wrong yet.

Bringing in electrical inspection experts to carry out a proper EICR before you commit to a purchase means having someone go through everything methodically, not just whatever’s easy to reach. They’ll work through:

- The consumer unit itself, whether it has proper RCD protection, and whether it’s actually up to the demands of a modern household

- Wiring condition throughout the building, including what’s running behind walls and under floors

- Every socket, switch, and light fitting in the property

- The earthing and bonding across the whole system

- Anything that points to overloading, deterioration, or work that someone did themselves at some point and probably shouldn’t have

Everything they find gets a grade. C1 is immediate danger, the sort that means the installation shouldn’t be used until it’s been dealt with. C2 is potentially dangerous, which still needs attention even if it hasn’t actually caused a problem yet. C3 is a recommendation rather than a requirement. Most properties that haven’t been inspected for a good while come back with at least one C2 on the report. Some come back with considerably more.

The cost of an EICR on a standard three-bedroom house sits between £150 and £300. Electrical Safety First estimates around 20,000 house fires in the UK every year are caused by electrical faults. The vast majority happen in homes where nobody knew anything was wrong, because nobody had checked.

Older properties carry more of this risk than newer ones. Houses wired before the 1970s may still have rubber-insulated cables that have gone brittle with age. Properties built before the 1950s sometimes still have lead-sheathed wiring in parts of the building that were never updated. Neither is acceptable in a modern installation, and both are worth knowing about before you complete rather than after.

If the seller has a recent EICR, ask to read the whole thing. Not to be told it exists or shown the front page, to actually read it. If there isn’t one, ask for an inspection to be carried out before exchange as a condition of the sale. A seller who won’t allow that is a seller worth thinking carefully about.

Plumbing Inspection

Water damage has a way of being worse than it first looks.

You open a wall expecting to find a failed joint and find instead that the moisture has been traveling along timbers for months, getting into places you didn’t expect, doing damage you can’t see from the outside. What looked like a contained problem turns into a much larger one, and the bill adjusts accordingly.

It’s also, oddly, one of the things buyers are least likely to check before they buy. A building survey will mention obvious damp if it’s staring back at the surveyor. It won’t tell you what’s going on inside the walls, whether the pipework is corroding behind the tiles, or whether the flexible hose connecting the washing machine to the supply has been there twice as long as it should have been.

Getting professional plumbing services to look properly at the system before you complete is the kind of thing that most buyers don’t think to do, and some of them later wish they had. A thorough inspection covers:

- Visible pipework for any early signs of corrosion, scale, movement at joints, or evidence of previous leaks that have been patched rather than properly fixed

- Stop valves and isolation valves, checking they actually turn rather than having seized at some point in the past and been left

- Water pressure and flow rate throughout the property

- The boiler and heating system, how old it is, whether it’s been serviced, and whether there are any signs of wear that suggest it’s near the end of its useful life

- The hot water cylinder or unvented system if the property has one

- Anywhere that looks like water damage might have been tidied up before viewings rather than actually dealt with

That last point is worth sitting with for a moment. A fresh patch of plaster in an otherwise dated bathroom. A ceiling that’s been repainted in a room where nothing else has been touched. These things might mean nothing. They might mean someone made something less visible before the property went on the market. An experienced plumber notices details like that. Someone doing their own walk-round often doesn’t.

There are a few things that come up repeatedly and tend to get missed:

- The boiler. Most have a working life of around 10 to 15 years. Replacement costs between £1,500 and £3,500. If the one in the property is getting on in age, that cost is sitting somewhere in your near future and it’s entirely reasonable to factor it into your offer.

- The heating system during viewings. Actually run it. Don’t take anyone’s word for it. Check that every radiator heats up properly, that the thermostat responds, and that the system behaves the way it should.

- The flexible hoses behind appliances. Washing machines, dishwashers, toilet cisterns. These hoses have a recommended service life of around five years. Most homeowners have never replaced them and couldn’t tell you how old they are. When one fails, it doesn’t drip. It lets go suddenly and completely, and it doesn’t stop until someone reaches the stopcock.

- Water pressure. Low pressure in one tap can be a minor nuisance. Consistently low pressure throughout the property can point to something more significant with the incoming supply or the internal pipework that isn’t a straightforward fix.

If the property is in Norfolk, hard water is worth factoring in specifically. The water hardness across most of the county is significant, and a boiler or heating system that’s never been treated for scale in those conditions is likely running less efficiently and may have less life left in it than its age alone suggests.

Drainage and Sewage

Properties on private drainage systems need a drainage survey. This is not a nice-to-have. If the property has a septic tank or treatment plant, you need to understand what you’re taking on before you take it on.

Regulations introduced in 2020 mean that certain older septic tanks discharging directly to watercourses are no longer legal and must be replaced or upgraded. If the property has one of these systems and it doesn’t comply, the cost and responsibility of sorting it out sits with the owner. After completion, that’s you, and it isn’t a small cost.

Even on mains-connected properties, a CCTV drainage survey is worth doing on anything older or anything that’s been extended. It shows the condition of the underground drainage, whether pipes are cracked, whether roots have found their way in, and whether everything flows where it’s supposed to. Underground drainage problems give no obvious warning until they’re serious, and serious drainage problems take time and money to sort out properly.

Planning and Building Regulations History

Has anything been built, converted, or structurally altered? If so, where’s the paperwork?

Extensions, loft conversions, garage conversions, and walls that have been removed all need the right consents. Your solicitor should check the planning history as standard, but it’s worth asking directly and specifically about any structural work you can see. If the paperwork is missing, find out why before you exchange rather than after.

Japanese Knotweed

It looks unremarkable. It can break through concrete, damage building foundations, and cause some lenders to decline the mortgage application entirely.

Ask the seller directly whether they’re aware of any knotweed on the property or adjoining land. Look carefully during viewings, particularly in borders and along boundaries. If there’s any genuine uncertainty, a specialist survey is available and worth commissioning. A professionally managed treatment plan is often what lenders require before they’ll proceed at all.

The Location Itself

Everything about the house can be changed eventually. The street it sits on cannot.

Go back at different times of day. Visit on a weekday morning and a Saturday evening. Both. Check the Environment Agency flood risk maps, which are publicly available, and find out whether the property falls within a meaningful risk zone. Look at whether any planning applications have been submitted nearby that might affect what gets built close to you in the next few years.

Talk to the neighbours if the opportunity arises. Not intrusively, just a brief conversation. The people who actually live on either side will tell you things about the street, the area, and the reality of day-to-day life there that no amount of viewings ever quite manages to convey.

Doing all of this takes time and costs money. It costs considerably less than buying a problem you didn’t know about because you didn’t look. The checks exist for a reason. Do them properly, do them before exchange, and go into the purchase knowing what you’re actually buying rather than what you hoped you were buying.