Why Retirement Planning Should Be About Life, Not Just Leaving a Bigger Portfolio

Retirement planning is often treated like a test of endurance.

Save more. Delay longer. Increase the success probability. End with the biggest portfolio possible. By that logic, the best retirement plan is the one that leaves behind the most money and takes the fewest risks along the way.

That sounds prudent. It can also produce the wrong life.

The problem with much traditional retirement planning is not that it is too cautious. It is that it often measures success by the wrong thing. A plan can be mathematically impressive and personally wasteful at the same time. It can create a 100% probability of financial success while quietly guaranteeing that the client works longer than necessary, delays meaningful experiences, and dies with far more money than was ever required to live well.

That is what “terminal wealth” planning too often does. It turns the end-of-life portfolio value into the primary scorecard, even though the real point of money was never to die with the highest number. The real point was to use money intelligently to support a meaningful life.

This is where a better retirement framework begins: not with “How much can I leave behind?” but with “What kind of life do I actually want this money to support?”

That shift matters more than it first appears. Once the question changes, so do the decisions. Travel sooner may matter more than preserving another million dollars at 92. Time with aging parents may matter more than another five years of over-saving. Giving, family memories, part-time work, flexibility and freedom may be more important than a Monte Carlo result that impresses the planner but does little for the client’s actual life.

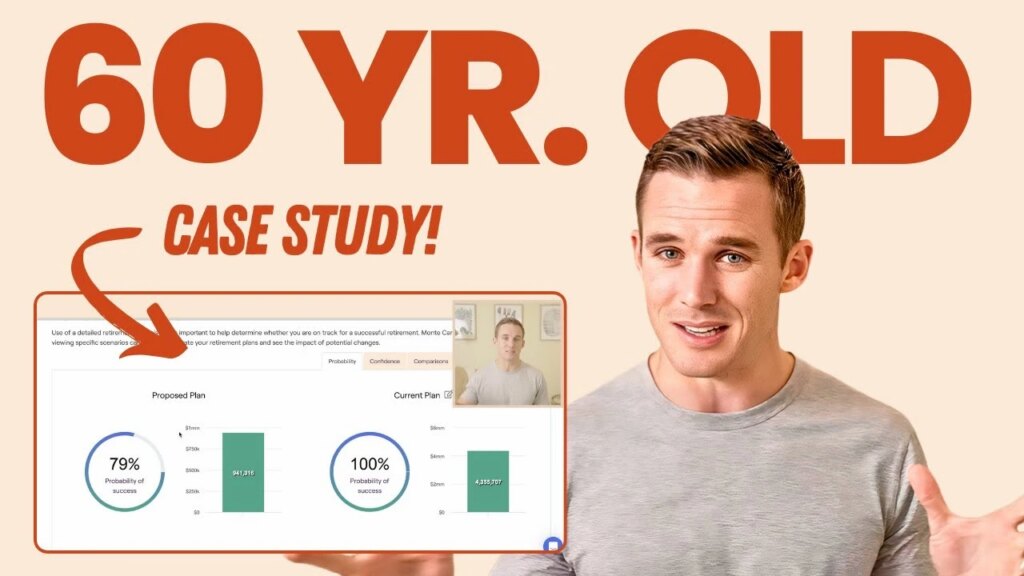

The case-study logic behind this outline makes the point clearly. A disciplined couple with a strong income, nearly $2.5 million in net worth and an already aggressive savings rate could project to a very large retirement portfolio if they kept doing exactly what they were doing. On paper, that looked like safety. In practice, it also looked like overaccumulation. The portfolio was already on track to support retirement needs comfortably, yet the household was still behaving as though every available dollar had to be pushed into the future.

That is where planning can become distorted. The plan starts serving the number rather than the person.

This often happens because people misunderstand what a 100% success probability really means. It does not mean “responsible.” It means “heavily buffered.” It means the plan contains more margin than may actually be needed, especially when the household already has meaningful fixed income, flexibility in spending, and options to adjust later. A 100% success rate sounds ideal, but it can also reflect a form of financial overprotection that extracts its own cost from life in the present.

That cost is opportunity cost, and it is one of the least discussed risks in retirement planning.

When people save aggressively beyond the point of necessity, they are not just accumulating wealth. They are also giving something up. Often it is time. Sometimes it is health. Sometimes it is the years when children are still at home, parents are still alive, or travel still feels easy. Those sacrifices rarely appear on a balance sheet. But they are no less real for being invisible.

This is why the right retirement plan is rarely the one with the biggest projected ending balance. It is the one that aligns money with values.

If the household wants $8,000 a month in retirement plus travel, and the assets already support that with a wide margin, then continuing to squeeze every possible dollar into retirement accounts may no longer be the highest and best use of money. That money could instead support life now, more time off, better experiences, more generosity, more family travel, more breathing room, without actually threatening the long-term plan.

Of course, this does not mean people should ignore risk. Retirement planning still requires discipline, realistic assumptions and periodic review. Markets can disappoint. Health can change. Spending can drift. Plans should be revisited and adjusted over time. But flexibility cuts both ways. It means retirees can tighten later if necessary. It also means they do not need to over-sacrifice now in the name of eliminating every possible future uncertainty.

That is the deeper flaw in overly conservative planning. It treats all risk as financial and too little of it as human.

There is real risk in underspending your healthiest years. There is real risk in delaying retirement until the people you wanted to spend time with are no longer there. There is real risk in assuming that because a portfolio can become $5 million or more, it therefore should. Sometimes the better decision is not to maximize assets but to use them sooner for the exact purposes that made saving worthwhile in the first place.

This is also why “failure” in retirement planning needs a more honest definition. If a plan has a lower statistical success probability but is backed by strong fixed income, flexible spending and modest downside severity, it may still be perfectly reasonable. The fear of anything less than total certainty can push people into years of unnecessary work and excess savings, even when the real-world consequences of a less-than-perfect scenario would be manageable. Retirement planning should not pretend every deviation from perfection is disaster.

A good plan should therefore answer two questions at once. First, can the money support the lifestyle? Second, is the lifestyle being delayed more than necessary in order to protect a number that may already be more than enough?

That second question is the one too many plans ignore.

Money is a tool. It is not the final objective. The purpose of retirement planning is not to produce the largest possible estate by default. It is to help people use resources intentionally, balancing security with living. That may include retiring earlier. It may include working part-time. It may include spending more now and saving slightly less later. It may include leaving less behind and enjoying more while you are here.

The right success metric is not whether the portfolio finishes as large as possible. It is whether the plan helped create the kind of life the client actually wanted.

Because the best retirement plan is not the one that dies richest. It is the one that lets you live fullest.

You should always consult a financial, tax, or legal professional familiar about your unique circumstances before making any financial decisions. This material is intended for educational purposes only. Nothing in this material constitutes a solicitation for the sale or purchase of any securities. Any mentioned rates of return are historical or hypothetical in nature and are not a guarantee of future returns.

Past performance does not guarantee future performance. Future returns may be lower or higher. Investments involve risk. Investment values will fluctuate with market conditions, and security positions, when sold, may be worth less or more than their original cost.