How to Earn $100,000 in Retirement and Pay $0 in Federal Taxes

It sounds too good to be true—but with the right planning, retirees can legally earn $100,000 a year and pay $0 in federal income taxes.

This isn’t about tax loopholes or fancy tricks. It’s about understanding how the IRS treats different income sources and layering them smartly to stay under key tax thresholds.

Let’s walk through how Joe and Sally, both retired at 67, make it happen—while enjoying a secure, tax-efficient retirement.

1. The Big Picture: $100,000 in Tax-Free Income

Joe and Sally’s plan includes income from:

- Social Security

- Qualified dividends

- Traditional IRA withdrawals

- Long-term capital gains

- Roth IRA for flexibility (but not needed for this specific plan)

They generate $100,000 per year by mixing these income sources—without triggering federal tax liability. Here’s how they do it.

2. Social Security and the Power of Provisional Income

Joe and Sally receive $62,400/year from Social Security ($3,200/month for Joe, $2,000/month for Sally).

Now here’s the trick: Social Security isn’t automatically taxable. It depends on provisional income, which includes:

- 50% of Social Security benefits

- Taxable IRA withdrawals

- Dividends and capital gains

At first, their provisional income is low enough that none of their Social Security is taxed. As they add other income, only $20,280 of it becomes taxable—which is still offset by deductions.

3. Dividend Income: Taxed at 0%

Their brokerage account (worth $500,000) produces $10,000/year in qualified dividends (2% yield).

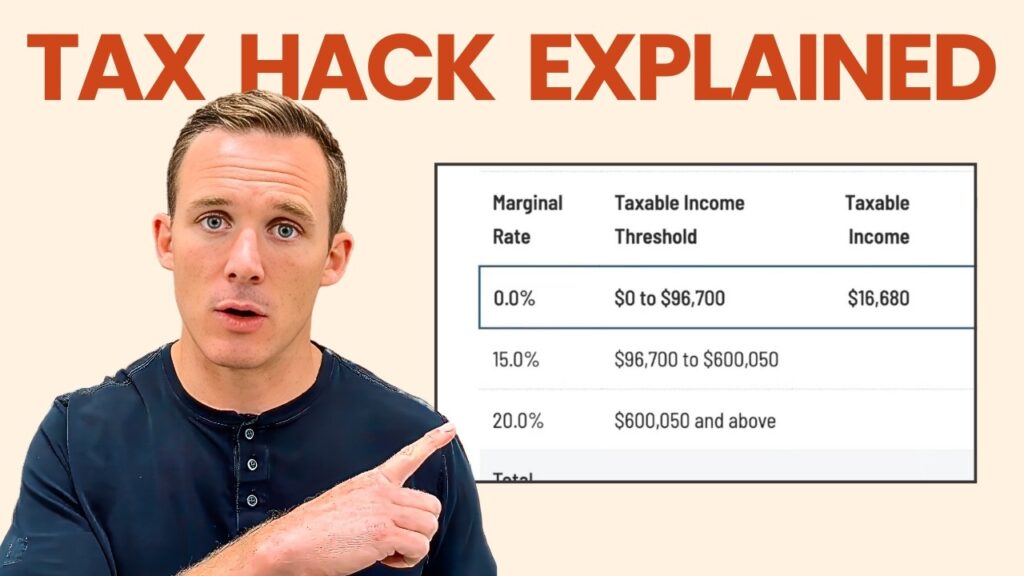

Because their taxable income remains under $96,700, they’re in the 0% capital gains tax bracket, meaning those dividends are taxed at 0%.

So, that $10,000 in dividend income? It’s all tax-free.

4. IRA Withdrawals: Keep It Modest

Joe and Sally also have $650,000 in traditional IRAs. To meet their spending needs, they withdraw $11,600/year—just enough to supplement income without inflating their taxable income too much.

Traditional IRA withdrawals are taxed as ordinary income—but here’s where the standard deduction comes in…

5. Using the Standard Deduction Wisely

As a married couple filing jointly in 2025, Joe and Sally can claim a $33,200 standard deduction (includes the 65+ senior bonus).

That means their $11,600 IRA withdrawal + $20,280 of taxable Social Security = $31,880 in taxable income—which is fully offset by the standard deduction.

Result? $0 in taxes owed.

6. Long-Term Capital Gains: More Tax-Free Income

To reach their $100,000 annual income target, Joe and Sally sell stocks for $8,000 in long-term capital gains each year.

As with their qualified dividends, these gains fall under the 0% long-term capital gains rate since their taxable income remains under the $96,700 threshold.

More income—still no taxes.

7. What About the Roth IRA?

They also have $150,000 in Roth IRAs, which can be tapped tax-free if needed. But in this scenario, they don’t need to use them. The Roth remains a great fallback option—especially if unexpected expenses arise or tax laws change.

8. Long-Term Strategy: Not Just One Year

While this plan focuses on the current year, the goal is broader: minimize taxes over their lifetime.

Key points of the long-term strategy:

- Keep taxable income low early in retirement

- Delay large IRA withdrawals until RMDs are required (at age 73+)

- Use Roth IRAs to bridge gaps if needed

- Consider Roth conversions in low-income years

- Monitor income thresholds to avoid triggering taxation on Social Security

This forward-looking mindset ensures Joe and Sally avoid tax surprises in later years—and stretch their nest egg further.

Final Thoughts: Planning Pays Off

Generating $100,000 a year in retirement with zero taxes owed isn’t luck. It’s the result of intentional planning:

- Mixing income types

- Staying below tax thresholds

- Maximizing the standard deduction

- Planning ahead for the next 20–30 years

With smart decisions today, you can enjoy more freedom, flexibility, and financial peace tomorrow.

You should always consult a financial, tax, or legal professional familiar about your unique circumstances before making any financial decisions. This material is intended for educational purposes only. Nothing in this material constitutes a solicitation for the sale or purchase of any securities. Any mentioned rates of return are historical or hypothetical in nature and are not a guarantee of future returns.

Past performance does not guarantee future performance. Future returns may be lower or higher. Investments involve risk. Investment values will fluctuate with market conditions, and security positions, when sold, may be worth less or more than their original cost.