Jeffrey Epstein’s Money Mystery: Where Did the Fortune Really Come From?

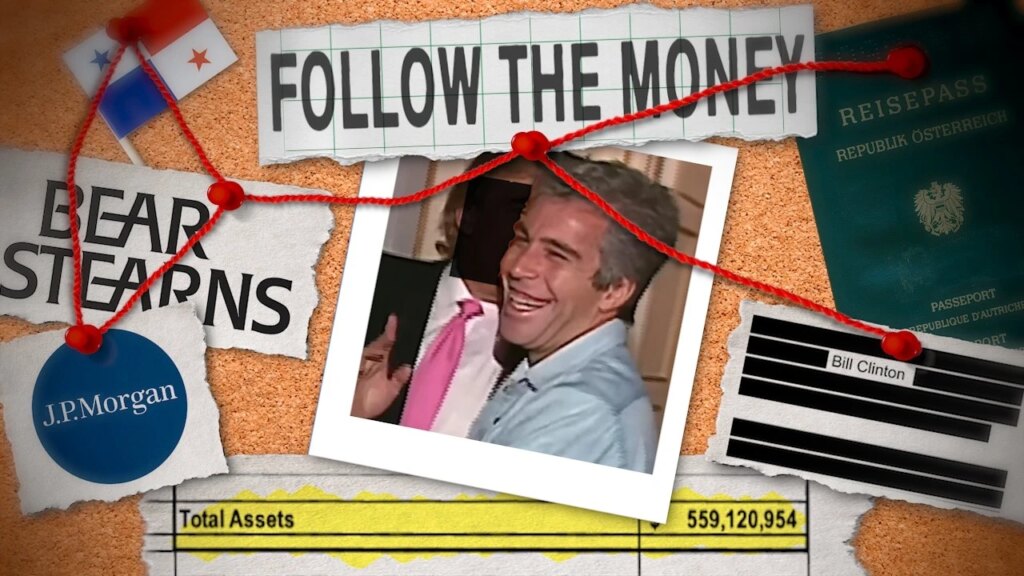

Jeffrey Epstein is often described as a “financier,” a man who moved through elite circles with the confidence of someone who belonged there. But the deeper you look into his financial story, the stranger it gets. Epstein left behind a will that reportedly listed roughly $577 million in assets, signed just days before his death. That number alone raises the question people still ask today: how did he actually make his money?

Because unlike most legitimate financial giants, Epstein’s career doesn’t read like a traditional Wall Street story built on credentials, track record, or transparent business success. Instead, it reads like a maze of relationships, private deals, offshore structures, and unanswered questions.

This isn’t just a story about a wealthy man. It’s a case study in how money can move through the modern financial system in ways that are difficult to trace, difficult to prove, and sometimes nearly impossible to fully understand from the outside.

The problem with the “financier” label

In the financial world, titles matter. Portfolio manager. Hedge fund founder. Private equity partner. Investment banker. These labels usually come with a paper trail: SEC filings, audited funds, investor letters, performance history, or at least a recognizable business model.

Epstein had something different: influence, proximity to power, and the reputation of someone who handled enormous wealth. Yet the public record never fully shows the kind of institutional structure that typically produces hundreds of millions of dollars in personal fortune.

And that’s why his wealth remains one of the most debated pieces of the Epstein story. If someone builds a fortune the conventional way, the math is easy to follow. Epstein’s math is not.

The early rise: Bear Stearns and a fast-track career

Epstein entered finance through Bear Stearns in the late 1970s, starting in a junior role and climbing quickly. According to the outline, he began as a coffee runner-type employee and became a limited partner by around 1980, a leap that would be unusual even for high-performing professionals with elite credentials.

It’s not impossible for someone to rise quickly in finance. But it’s rare without a clear specialization, standout deal flow, or some kind of client network that immediately generates serious revenue.

That’s the first puzzle: Epstein’s early rise appears less like a traditional merit-based climb and more like a relationship-based acceleration. In a world where access is often more valuable than expertise, that distinction matters.

The “relationship banker” model: power, proximity, and private leverage

If Epstein wasn’t building wealth through a widely visible investment track record, the next logical explanation is that he built wealth by becoming useful to the wealthy.

There is a type of financial operator who doesn’t need to be the best investor. They need to be the person who knows how to solve problems quietly. That could mean introductions, structuring, asset protection, tax minimization, crisis management, or moving money efficiently across jurisdictions.

This is where Epstein’s story begins to resemble the darker edge of high-net-worth finance, where “services” can mean almost anything, and fees are justified not by performance but by discretion.

In that world, the product isn’t investing. The product is access, secrecy, and control.

Charging elite-level fees without elite-level transparency

The outline highlights something critical: Epstein reportedly charged extremely high fees while providing services he was not clearly credentialed to deliver, including tax strategy and wealth management. In a regulated environment, that would raise immediate red flags.

But when the client is ultra-wealthy, and the relationship is private, the normal consumer protections don’t apply the same way. These are not people filing complaints with the Better Business Bureau. These are people who often want fewer eyes on their financial lives, not more.

That creates the perfect environment for a business model built on ambiguity.

If a wealthy client pays tens of millions in “fees,” the question becomes: fees for what, exactly?

And when that question can’t be answered clearly, it opens the door to the suspicion that the financial work wasn’t the full story.

Towers Financial and the shadow of a Ponzi ecosystem

One of the most alarming points in the outline is the connection to Towers Financial Corporation, described as a Ponzi scheme that cost investors roughly $450 million. If Epstein was involved in that ecosystem, it adds another layer to the broader narrative: proximity to high-risk, high-opacity financial operations.

Ponzi schemes don’t survive because they are brilliant. They survive because they use credibility as currency. They create the illusion of legitimacy long enough to attract money, and they often rely on insiders who understand how to sell trust.

Even being adjacent to that world tells you something important: Epstein’s financial environment wasn’t built like a standard advisory firm. It appears to have operated in the grey space between wealth management, influence, and financial manipulation.

The offshore advantage: why the Virgin Islands mattered

One of the clearest financial moves in Epstein’s story was shifting operations offshore, particularly into the U.S. Virgin Islands. Offshore jurisdictions exist for a reason: they reduce taxes, reduce scrutiny, and increase flexibility in how money is structured and moved.

Even when offshore strategies are technically legal, they often make it harder for outsiders to see what is really happening. That’s not an accident. That’s the feature.

The outline suggests Epstein benefited from favorable tax structures and lower effective rates than would be expected in New York. That matters because if you’re generating major revenue, where you book it can change everything.

It can change how much tax you pay.

It can change what regulators can see.

It can change what courts can access.

It can change how clients are documented.

It can change how assets are held and protected.

For someone whose business depended on secrecy, offshore structuring wasn’t a side detail. It was central to the operating model.

The missing pieces: why the fortune doesn’t fully add up

The outline points out another key issue: only about half of Epstein’s reported wealth was tied to cash-generating assets. That’s not how most self-made fortunes look.

If someone is worth hundreds of millions, you typically expect to see:

A large equity stake in a company

A portfolio of income-producing real estate

A hedge fund track record and carried interest

Public market holdings and a clear investment strategy

A business with recurring revenue

Instead, what you see here is a wealth figure that appears large, but not fully explained by visible income streams. Add in the costs of Epstein’s lifestyle and extensive legal expenses, and the financial picture becomes even harder to reconcile.

When the money doesn’t match the model, analysts start looking for hidden variables.

And in Epstein’s case, those hidden variables may have been the entire story.

The client list problem: who was paying, and why?

Epstein’s connections to major names like Les Wexner and Leon Black are often referenced in discussions of his wealth. But the outline raises an uncomfortable reality: it’s not always clear what clients were paying for.

In legitimate wealth management, fees are tied to:

Assets under management

A percentage of performance

A flat planning fee

A clearly defined advisory scope

But Epstein’s alleged earnings were reportedly enormous, and the structure of those fees has long been difficult to explain through traditional advisory math.

When payments are large and the service is unclear, the natural suspicion is that the transaction wasn’t purely financial. It may have been about influence, leverage, or protection.

Because in the world of the ultra-wealthy, money is sometimes used to buy more than returns.

It’s used to buy silence.

It’s used to buy loyalty.

It’s used to buy control.

Transactions linked to sanctioned banks: the global finance warning sign

The outline notes financial transactions connected to banks that later became sanctioned Russian institutions. That detail matters because it points toward the kind of cross-border complexity that is extremely difficult to untangle, even for investigators.

Global finance can be legitimate, but it can also be used to obscure:

Source of funds

Ownership

Purpose of transfers

Beneficial recipients

Tax obligations

When money moves through offshore structures and international banking networks, it becomes harder to determine what is business income, what is hidden compensation, and what is something else entirely.

And when secrecy is the goal, complexity becomes the tool.

What Epstein’s case reveals about modern finance

Even without speculating beyond the outline, Epstein’s financial story highlights something that’s true far beyond one individual:

The financial system has areas where wealth can exist without transparency.

It can be built through private relationships instead of public performance. It can be structured through offshore vehicles that reduce visibility. It can move through systems that reward complexity and punish outsiders trying to follow the trail.

That’s why Epstein’s fortune remains such a disturbing financial mystery. Not because it’s impossible to understand wealth, but because it demonstrates how wealth can be engineered in ways that resist understanding.

The real takeaway: follow the structure, not the story

When people hear “financier,” they assume investments, portfolios, and market skill. Epstein’s story suggests something different: a financial structure built on access, discretion, and private power.

That doesn’t automatically answer every question about where his money came from. But it explains why the public has never received a clean explanation.

Because in a normal financial life, the money trail is the proof.

In Epstein’s world, the money trail was the thing designed to disappear.

Final thoughts

Jeffrey Epstein’s wealth wasn’t just a number on a balance sheet. It was a signal of how deeply embedded he was in a system where money, influence, and secrecy can overlap.

His will, his offshore positioning, his unclear fee structure, his high-profile client network, and the lingering gaps in how his fortune was built all point to the same conclusion: the story of Epstein’s money is not a typical wealth story.

It’s a modern finance story. One where the biggest questions aren’t about returns, but about relationships, leverage, and what people are willing to pay for behind closed doors.

And until the full structure is exposed, the mystery isn’t going away.

All writings are for educational and entertainment purposes only and does not provide investment or financial advice of any kind.