The Hidden Traps of Roth Conversions: How to Maximize Tax-Free Retirement Without Triggering Costly Surprises

Roth conversions are one of the most powerful retirement planning tools available—but they can also be one of the most misunderstood. If done strategically, converting traditional IRA dollars to Roth can reduce your lifetime tax burden and leave more for your heirs. But if done carelessly, it can trigger hidden traps that cost you thousands in unnecessary taxes and surcharges.

Let’s break down how to avoid the pitfalls—and how one couple, Bob and Sally, turned a good Roth conversion strategy into a great one.

1. Roth Conversions and Tax Bracket Management

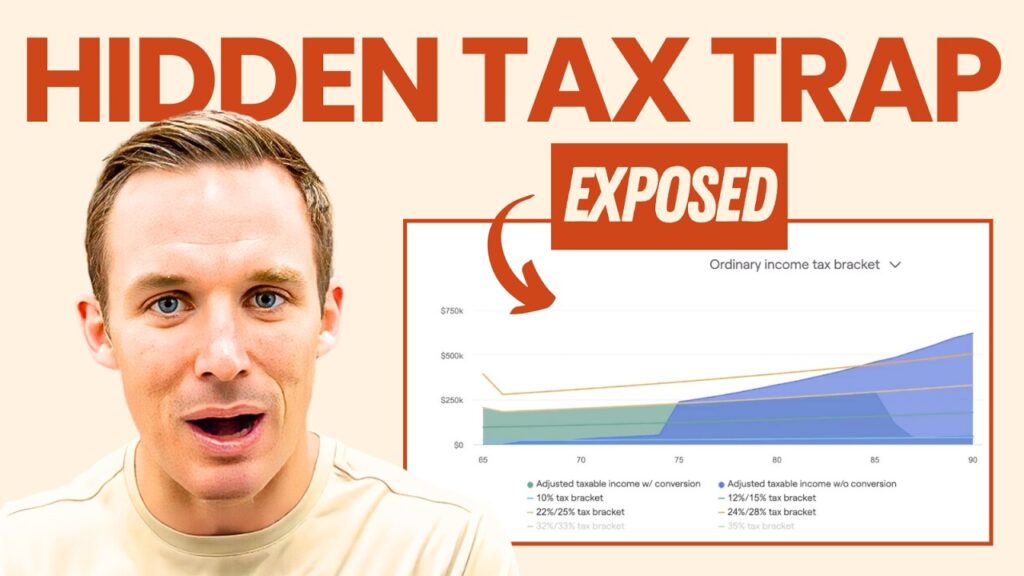

Many advisors recommend doing Roth conversions up to a certain tax bracket—like 10%, 12%, or 22%—to “fill the bucket” without spilling over into higher brackets like 24% or 32%.

Why? Because later in retirement, Required Minimum Distributions (RMDs) can push you into a higher tax bracket. That’s exactly what was projected to happen for Bob and Sally. Converting early at a lower rate would reduce their taxable IRA balances and lower future RMDs.

Initially, they planned to convert up to the 22% bracket. This approach saved them an estimated $485,000 in tax-adjusted portfolio value by age 90—already a win. But it could’ve been better.

2. Beware of the IRMA Surcharge Trap

What Bob and Sally didn’t expect? Their Roth conversions bumped their Modified Adjusted Gross Income (MAGI) just $1 over the IRMA threshold—triggering higher Medicare premiums.

The Income-Related Monthly Adjustment Amount (IRMAA) increased their Medicare Part B and D costs by $5,828 annually.

But that’s not all. Because they had to withdraw extra funds from their IRA to cover those healthcare surcharges, the opportunity cost over 25 years was an estimated $47,000 in lost investment growth.

Just one dollar over the limit created a compounding penalty that turned a good tax strategy into an expensive oversight.

3. A Better Strategy: Stay Below IRMA

Once they revised their approach and aimed just under the IRMA threshold, Bob and Sally saw huge gains.

Instead of converting all the way to the 22% tax bracket, they converted slightly less—but avoided IRMA surcharges. That small adjustment increased their projected portfolio value from $485,000 to $760,000.

Why the jump?

- Lower healthcare costs

- More assets left in their accounts to compound

- Better overall tax efficiency

Sometimes converting less can mean keeping more.

4. The Other Hidden Taxes of Roth Conversions

IRMA surcharges aren’t the only danger. A Roth conversion also affects:

- Social Security “tax torpedo”: Increases in provisional income can make up to 85% of your Social Security benefits taxable.

- Capital gains taxes: Higher MAGI can push long-term capital gains and dividends from 0% to 15% or even 20%.

- Your heirs’ tax brackets: If your beneficiaries are in lower tax brackets, they might have paid less tax on inherited traditional IRA dollars than you will converting them now.

Every tax lever affects another—and ignoring that can lead to thousands lost.

5. The Case for Comprehensive Roth Planning

Smart Roth conversion planning involves more than just your current tax bracket. It means understanding:

- IRMA thresholds

- Social Security taxation

- Capital gains interaction

- Future tax rates for your heirs

- Portfolio growth expectations

- Medicare costs

Many retirees benefit from using retirement planning software or working with a financial planner who models these interactions. At the very least, understanding where each tax trap lives on the map gives you a fighting chance.

6. Final Takeaways

If you’re doing Roth conversions—or thinking about them—keep these takeaways in mind:

- Roth conversions are powerful, but precision matters.

- IRMA surcharges can turn small missteps into expensive, recurring costs.

- Consider all the tax interactions, not just income taxes.

- Legacy planning and Medicare costs should factor into your strategy.

- A little foresight could mean hundreds of thousands in extra retirement dollars.

The right Roth strategy is less about brute force and more about finesse. Get it right, and your future self—and your heirs—will thank you.

You should always consult a financial, tax, or legal professional familiar about your unique circumstances before making any financial decisions. This material is intended for educational purposes only. Nothing in this material constitutes a solicitation for the sale or purchase of any securities. Any mentioned rates of return are historical or hypothetical in nature and are not a guarantee of future returns.

Past performance does not guarantee future performance. Future returns may be lower or higher. Investments involve risk. Investment values will fluctuate with market conditions, and security positions, when sold, may be worth less or more than their original cost.