Why Retirement Is Harder for Single Women

Retirement planning is often framed as a numbers exercise how much you’ve saved, how much you’ll spend, and whether the math works. For single women, however, the equation is more complicated. The challenge isn’t simply having enough assets. It’s that the underlying assumptions many financial plans rely on were built for couples, not individuals navigating retirement alone.

One of the most persistent, and costly, mistakes is the belief that a single person’s expenses should be roughly half those of a married household. At first glance, the logic appears sound. In reality, it breaks down quickly. Housing costs, which represent one of the largest expenses in retirement, rarely scale down proportionally. Property taxes, insurance, utilities, and maintenance remain largely fixed regardless of how many people live in the home. A single retiree often carries nearly the same baseline costs as a couple, but with only one income stream to support them.

That imbalance extends beyond housing. The tax code is less forgiving to single filers, who face a smaller standard deduction and reach higher marginal tax brackets at lower income levels than married couples. At the same time, Social Security provides fewer options. While married retirees can coordinate spousal and survivor benefits, single individuals are typically limited to their own work history, leaving less flexibility to optimize income over time.

The result is a narrower margin for error. Without a second income or shared expenses, financial missteps carry greater consequences, and unexpected costs, particularly in healthcare, can place disproportionate strain on a single retiree’s portfolio.

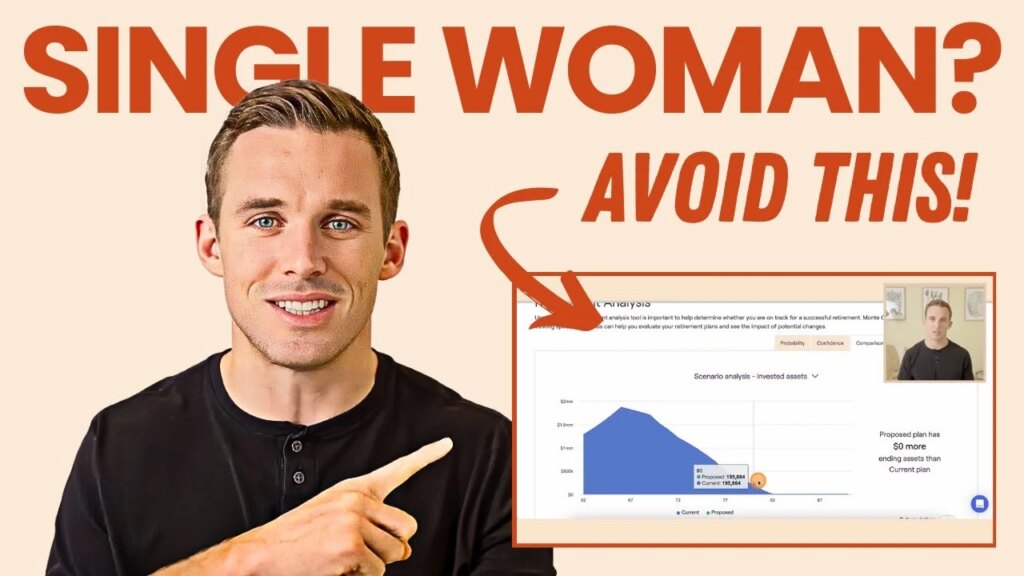

A case study illustrates how these dynamics play out. Consider a recently divorced 63-year-old woman with approximately $1.3 million in liquid assets and significant home equity. Her goal is straightforward: retire at 67, maintain a comfortable lifestyle with monthly expenses of about $6,000, travel regularly, and contribute to her grandchildren’s education. On paper, her financial position appears strong.

But when projected expenses are fully accounted for including discretionary spending and inflation—the gap between income and spending widens considerably. To sustain her lifestyle, she would need to withdraw roughly 9% annually from her investment portfolio. That rate, well above conventional sustainability thresholds, would likely deplete her liquid assets within two decades.

The issue isn’t a lack of resources. It’s a mismatch between assumptions and reality.

The most effective adjustments are often structural rather than incremental. In this case, housing emerges as the pivotal variable. By selling a high-value home in a costly market and relocating to a lower-cost region, the retiree could unlock substantial equity, reduce property taxes, and lower ongoing expenses. That single decision reshapes the entire financial plan, reducing withdrawal rates and extending portfolio longevity.

Such changes highlight a broader principle: retirement planning for single individuals demands flexibility and personalization. Unlike couples, who must align decisions across two people, single retirees can adapt more quickly to changing circumstances. This flexibility can be a significant advantage if it is used intentionally.

Tax strategy is another critical lever. For individuals in high-tax states, reallocating contributions from Roth accounts to tax-deferred vehicles can improve near-term cash flow and reduce overall tax liability. When combined with geographic relocation, these adjustments can materially improve long-term outcomes.

Social Security decisions also carry added weight. Divorced or widowed individuals may have access to benefits based on a former spouse’s earnings record, but these options require careful timing and a clear understanding of eligibility rules. Optimizing these benefits can increase monthly income meaningfully, but the window for making those decisions is finite.

What often goes overlooked is the psychological dimension of retirement planning. Many individuals continue to operate under financial assumptions tied to a previous stage of life most commonly, a marriage that no longer exists. Without revisiting and updating those assumptions, even well-funded plans can fall short.

The broader lesson is that retirement planning is not static. For single women in particular, success depends less on following standardized formulas and more on building a strategy that reflects their current reality. Fixed costs, tax exposure, and income constraints must all be evaluated on their own terms, rather than adjusted versions of a couple’s framework.

Done correctly, this approach doesn’t just reduce risk. It creates optionality. It allows for earlier retirement, greater spending flexibility, and a more intentional allocation of time and resources.

Retirement, in this context, is not about cutting back to make the numbers work. It is about aligning financial decisions with the life you actually intend to live and ensuring the structure behind those decisions can support it.

You should always consult a financial, tax, or legal professional familiar about your unique circumstances before making any financial decisions. This material is intended for educational purposes only. Nothing in this material constitutes a solicitation for the sale or purchase of any securities. Any mentioned rates of return are historical or hypothetical in nature and are not a guarantee of future returns.

Past performance does not guarantee future performance. Future returns may be lower or higher. Investments involve risk. Investment values will fluctuate with market conditions, and security positions, when sold, may be worth less or more than their original cost.