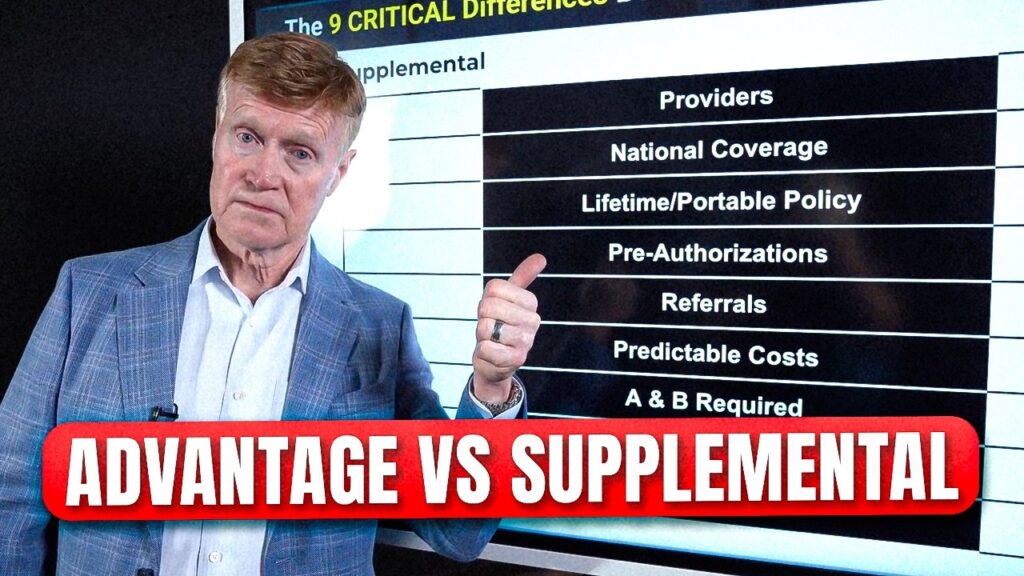

9 Biggest Differences Between Medicare Supplement and Medicare Advantage

Choosing Medicare is often presented as a matter of comparing premiums and picking the cheapest option. In reality, the decision is far more consequential. The two main paths—Medicare Supplement plans and Medicare Advantage plans—can lead to very different experiences when it comes to doctor access, travel, approvals, budgeting, and long-term flexibility.

That is why the choice deserves to be framed less as a product comparison and more as a structural decision about how you want healthcare to work in retirement. Both approaches can provide coverage. But they do not operate the same way, and the differences can become especially important as health needs grow more complex.

Here are the nine biggest differences between Medicare Supplement and Medicare Advantage.

1. Provider access

The clearest difference is access to doctors and hospitals. Medicare Supplement plans work alongside Original Medicare, which is widely accepted across the country. That means beneficiaries can generally see any provider that accepts Medicare without worrying about whether that doctor is inside a private insurance network. Medicare Advantage plans, by contrast, typically operate through HMO or PPO networks, which can limit provider choice and create higher costs for out-of-network care.

For many retirees, this is the difference that matters most. A Supplement plan is built around flexibility. An Advantage plan is built around managed networks.

2. Travel flexibility

Coverage on the road is another major dividing line. Because Supplement plans pair with Original Medicare, they are much easier to use nationwide. Advantage plans are often designed around local or regional service areas. Emergency and urgent care are generally covered either way, but routine care outside the home region can become more difficult or more expensive under an Advantage plan. For retirees who travel often, split time between states, or expect to move, that distinction can matter a great deal.

3. Policy permanence and portability

Supplement plans are generally designed as long-term coverage. They are portable if you move, and once you have the policy, it is intended to continue rather than reset every year. Advantage plans work more like annual contracts. They can change from year to year, and if you move to another area, you may need to choose a different plan. That makes Supplement coverage feel more stable over time, while Advantage can require more recurring plan management.

4. Pre-authorization requirements

One of the biggest frustrations beneficiaries can face is the need to get approval before receiving certain services. Supplement plans typically do not impose much of this friction because once Medicare pays its share, the Supplement plan is generally designed to cover the remaining approved amount. Advantage plans often require pre-authorization for higher-cost services such as surgeries, scans, or extended care. That can mean more paperwork, more waiting, and in some cases denials or delays.

This is not a small administrative issue. It can shape how easy or difficult it feels to use your healthcare.

5. Referrals to specialists

With a Supplement plan, beneficiaries can usually see specialists directly as long as the provider accepts Medicare. Advantage plans, especially HMOs, often require a referral from a primary care doctor before specialist care is covered. That added step may not sound dramatic, but over time it can become one more layer of gatekeeping between the patient and the care they want.

6. Cost predictability

This is where many retirees split philosophically. Supplement plans usually cost more each month in premiums, but in exchange they offer a more predictable structure. Once the premium is paid and the Medicare Part B deductible is met, coverage is generally quite comprehensive. Advantage plans often advertise low or even zero additional premiums, but that does not mean care is free. Costs arrive in the form of copays, coinsurance, and service-based charges.

In other words, Supplement plans tend to trade higher fixed cost for lower surprise. Advantage plans tend to trade lower monthly premiums for more variable out-of-pocket exposure.

7. Out-of-pocket risk

Advantage plans do have an annual out-of-pocket maximum, which places a ceiling on the year’s spending, but that maximum can still be significant. Supplement plans are often designed to fill most of the major gaps left by Medicare, making the retiree’s exposure feel more contained once the premium and deductible are handled. This is one reason retirees who want cleaner budgeting often lean toward Supplement coverage, while those more comfortable with pay-as-you-go risk may consider Advantage.

8. Monthly premiums and tradeoffs

A common misconception is that one option is simply cheaper than the other. The reality is more nuanced. Supplement plans require monthly premiums because they are designed to cover many of Medicare’s gaps. Advantage plans often come with little or no extra premium from the insurer, but beneficiaries still remain responsible for Medicare Part B and can face additional costs throughout the year when services are used. The real question is not whether you pay, but how you prefer to pay: upfront through premiums or later through service-based charges.

9. Extra perks and benefits

Advantage plans often promote extras such as dental, vision, hearing, or wellness benefits. Supplement plans generally do not focus on these perks and are designed more narrowly around medical coverage. For some beneficiaries, the extras are genuinely attractive. For others, they can become a distraction from the more important structural issues like provider access, approvals, and long-term flexibility.

That is really the heart of the Medicare decision. One path tends to prioritize broad access, portability, and predictability. The other tends to emphasize lower premiums and added perks, but with more network rules, more utilization controls, and more variable costs.

Both options can work. But they do not work in the same way, and they are not best judged by the monthly premium alone. The right answer depends on how much flexibility you want, how often you travel, whether you are comfortable managing referrals and approvals, and how much uncertainty you are willing to accept in exchange for lower fixed costs.

That is why this choice is so important, especially at age 65. A Medicare decision is not just about getting from point A to point B. It is about deciding what kind of healthcare experience you want for the years ahead. And once you understand the nine biggest differences, the decision becomes much clearer.