Why Retirement Planning Should Start With Spending, Not Investing

Most people approach retirement backward.

They start with the portfolio. How much is in the 401(k)? How much is in the IRA? Is the balance big enough? Should the money be in stocks, bonds, or cash? Those questions matter, but they are not the first ones that should be asked.

The first question is simpler and more important: what does life actually cost?

That is because retirement is not funded by account balances in the abstract. It is funded by spending. And the people who retire well are usually not the ones who only accumulated the most. They are the ones who understand how to turn their resources into a sustainable income stream that fits the life they want to live.

That means retirement planning should begin with spending, not investing.

The reason is practical. A retiree does not wake up each month and spend “net worth.” They spend on housing, food, healthcare, utilities, travel, hobbies, family support, taxes, and the occasional surprise. Until those outflows are understood, the portfolio is just a pile of assets without a job description.

This is why reviewing actual spending matters so much.

Not rough guesses. Not what someone hopes retirement will cost. The best starting point is usually the last six months of bank and credit card statements. That creates a clearer picture of where money is really going. Once that is visible, expenses can be divided into needs, wants, and wishes. Needs are the core obligations that have to be covered no matter what. Wants are the flexible parts of life that make retirement enjoyable but can be adjusted. Wishes are the bigger extras, gifts, legacy goals, special trips, one-time projects, or charitable ambitions that should be planned for separately.

That distinction matters because retirement spending should not be rigid.

One of the biggest mistakes people make is assuming retirement spending is flat. It rarely is. Some expenses are stable, but many are flexible and should respond to market conditions and changing life stages. Spending may be higher early in retirement when people are more active, lower in the middle years, and then rise again later with healthcare or support needs. A good retirement plan makes room for that reality instead of pretending every year looks the same.

Once spending is clear, the next step is to line up income.

Retirees often have more moving parts than they realize. Social Security, pensions, annuities, part-time work, rental income, dividends, and portfolio withdrawals may all play a role. The goal is to coordinate them, not just list them. Once those income sources are measured against expected spending, the real pressure on the portfolio becomes easier to see.

That is the critical number.

Not the total account balance, but the gap between what outside income covers and what still has to come from investments. That gap is what determines how much risk the portfolio really needs to support. Two retirees with the same $2 million balance may have completely different outcomes depending on whether one needs to withdraw $20,000 a year and the other needs $90,000.

This is why the 4% rule, while useful, is often misused.

The rule is popular because it is simple. Withdraw 4% in the first year, adjust for inflation, and assume the money lasts around 30 years. As a rule of thumb, it has value. As a complete retirement strategy, it is too blunt. It ignores taxes, ignores the different treatment of account types, ignores that spending changes over time, and ignores that retirees can often adapt rather than keep withdrawals fixed no matter what markets do.

That flexibility is not a small detail. It is one of the most important strengths a retiree has.

A better retirement plan behaves more like a paycheck than a formula. It covers recurring expenses, adjusts to conditions, and is built with tax awareness from the beginning. That is where withdrawal sequencing becomes so important. Not all retirement dollars are equal. Money coming from a taxable brokerage account behaves differently from money coming out of a traditional IRA. Roth accounts behave differently again. Social Security can also be taxed, and required minimum distributions can create ugly surprises later if no one planned ahead.

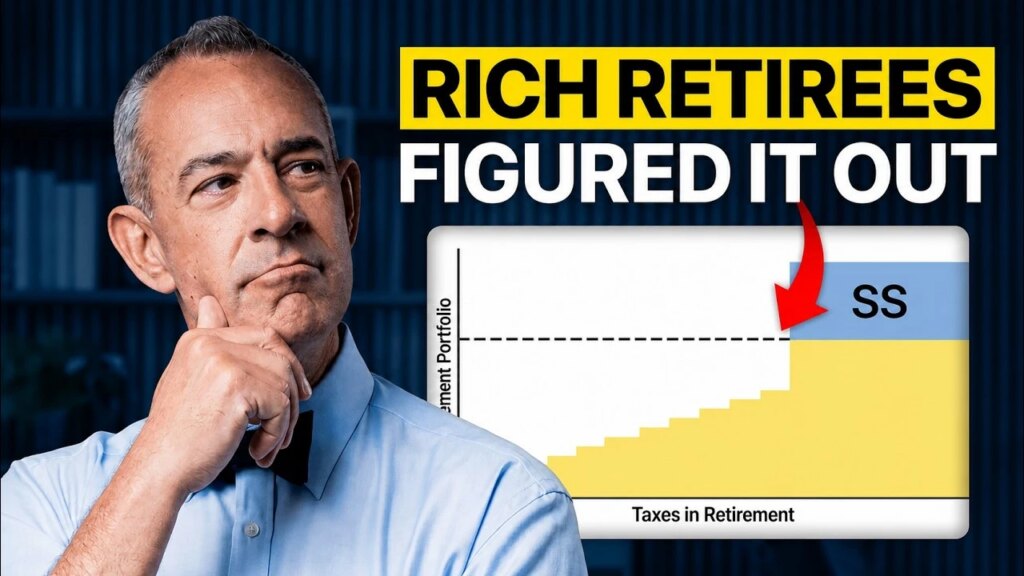

Taxes are one of the quietest ways retirement income gets damaged.

A retiree can have strong savings and still net far less than expected if withdrawals are handled poorly. Up to 85% of Social Security benefits can become taxable. IRA withdrawals are taxed as ordinary income. Required minimum distributions can force income higher than needed in a given year, pushing up taxes and sometimes Medicare premiums too. That is why the order in which money is withdrawn matters almost as much as the amount.

A thoughtful plan does not just ask, “How much do I need?” It asks, “Where should it come from first?”

That is also why Roth conversions often become part of the conversation before retirement. Moving some money from pre-tax accounts into Roth accounts during lower-income years can reduce future tax pressure and create more flexibility later. A retiree with access to taxable, tax-deferred, and tax-free accounts has far more control than one relying heavily on only one bucket.

The investment structure should then support that paycheck.

This is where a total-return approach becomes more useful than a narrow income-only mindset. Many retirees instinctively look for income-producing assets alone, but retirement portfolios usually work better when they are built in layers. Short-term reserves can cover one to three years of expected spending in lower-risk holdings. Intermediate assets such as bonds can generate income and replenish those reserves. Long-term growth assets such as stocks can continue compounding and protect purchasing power against inflation.

That layered design solves a major problem: sequence risk.

If markets fall early in retirement, a retiree forced to sell stocks immediately may damage the portfolio far more than someone who can live on reserves and let growth assets recover. The purpose of the reserve is not to avoid investing. It is to buy time. That makes the portfolio more durable and the retiree less likely to make panicked decisions during downturns.

This is why retirement success depends less on how much was saved than on how efficiently the money is used.

A retiree does not need a perfect portfolio. They need a coordinated system. One that understands spending, lines up income, manages taxes, adjusts to reality, and invests with enough structure that market swings do not turn into lifestyle crises.

That is the real point of retirement planning.

Not simply to hit a number, but to create a reliable, flexible paycheck from the assets you spent decades building.

And that process starts with spending, because until you know what the money is supposed to do, you cannot know how well the portfolio is actually prepared to do it.

Intended for educational purposes only. Opinions expressed are not intended as investment advice or to predict future performance. Past performance does not guarantee future results. Neither the information presented, nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. Consult your financial professional before making any investment decisions. Opinions expressed are subject to change without notice.

IMPORTANT DISCLOSURES:

• Investment Advisory and Financial Planning Services are offered through Pure Financial Advisors, LLC. A Registered Investment Advisor.

• Pure Financial Advisors, LLC. does not offer tax or legal advice. Consult with a tax advisor or attorney regarding specific situations.

• Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

• Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

• All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy.

• Intended for educational purposes only and are not intended as individualized advice or a guarantee that you will achieve a desired result. Before implementing any strategies discussed you should consult your tax and financial advisors.