How is Everything Outpacing Inflation at the Same Time?

If you have looked at recent inflation headlines and thought they do not match your real life, you are not imagining it. Official numbers may say inflation has cooled, but for many households, daily life still feels relentlessly expensive. Groceries feel heavier on the budget. Housing feels further out of reach. Cars, insurance, healthcare, subscriptions, and basic services all seem to cost more than people expect. That disconnect between the statistics and lived experience has become one of the defining frustrations of the modern economy.

Part of the problem is that inflation is not a simple number describing one universal reality. It is a weighted average built from a basket of goods and services. Some prices rise quickly. Others rise slowly. Some even fall. When economists or government agencies report that inflation is running at a certain annual rate, they are describing the movement of that basket as a whole, not the exact cost pressures felt by every family. That means the headline figure can be technically true while still feeling emotionally and financially incomplete.

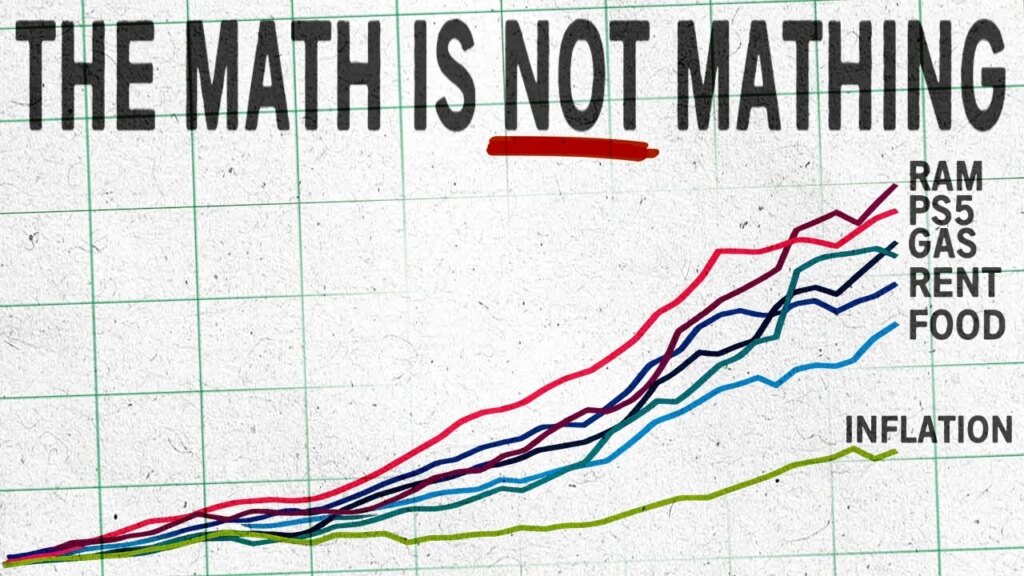

That gap becomes even more noticeable when the categories rising fastest are the ones people care about most. Essentials such as housing, healthcare, education, insurance, and major household purchases often matter far more to families than categories that may be flat or falling. A cheaper television does not offset a more expensive apartment. A better smartphone does not cancel out higher grocery bills, rising car insurance, or a jump in utility costs. Inflation may be slowing on paper while the most important parts of life remain stubbornly unaffordable.

One reason this happens is because inflation measurement includes quality adjustments. If a product becomes more advanced over time, statistical methods may treat part of the price increase as an improvement rather than pure inflation. In theory, that makes sense. A computer today is far more capable than one from a decade ago. But for consumers, the out-of-pocket reality still matters. If the sticker price is higher, the household budget feels the strain regardless of whether economists view some of that increase as a quality upgrade. That can make official inflation look softer than what people actually experience at checkout.

The issue becomes even more frustrating when products are not actually getting better. In many areas, people feel they are paying more for lower quality. Packages get smaller. Materials feel cheaper. Customer service gets worse. Devices become harder to repair. Software updates slow older products down and push people toward replacement. Companies cut costs while holding or raising prices, and consumers are left with the same bill for a worse experience. This is part of why so many people feel that inflation understates the real decline in value they are getting for their money.

Housing is one of the clearest examples of the mismatch between statistics and real life. Housing is the largest category in most inflation indexes, but it is measured indirectly. Instead of tracking home prices themselves, the official methodology leans heavily on something called owner’s equivalent rent, which estimates what a homeowner would theoretically pay to rent their own home. That approach may work for certain statistical purposes, but it can feel detached from reality when actual home prices, mortgage rates, insurance, property taxes, maintenance, and HOA costs are all moving in painful ways. For someone trying to buy or carry a home, the cost of housing can feel much higher than the official inflation treatment suggests.

This matters because housing is not just another item in the basket. It is often the biggest expense in a family budget. When housing costs rise sharply, it changes everything else. It reduces flexibility, squeezes savings, and limits the ability to absorb rising costs in other areas. And because official housing measurement can lag actual market conditions, the data may not fully capture what buyers and even many renters are feeling in real time.

Then there is the modern pricing environment itself. It is no longer as simple as walking into a store and seeing one clear price. More and more businesses use dynamic pricing, app-based discounts, bundles, personalized offers, and algorithmic adjustments that make the true cost of something harder to pin down. Two different consumers may pay two different prices for a similar product or service based on timing, shopping behavior, location, or digital profile. Busy people often pay more because they do not have the time to hunt through apps, comparison tools, or temporary promotions. That creates a sense that the economy is full of hidden price discrimination, because in many ways it is.

Subscription models add another layer. Many goods and services that used to be purchased once are now structured as recurring payments. Entertainment, software, shipping perks, news, storage, food delivery, home security, and even some vehicle features can become monthly line items. Each individual cost may look manageable, but together they create a budget that feels constantly under pressure. Inflation may not fully capture the psychological and financial drag of a life increasingly organized around recurring charges.

There are also broader structural reasons people feel squeezed. Healthcare, housing, and education have risen faster than general inflation for years. Energy prices still ripple through transportation and goods. Tariffs and trade policy can quietly raise the prices of imported items. Data practices and digital market structures create inefficiencies and hidden costs. These are not always visible in a single inflation print, but they shape the financial lives people actually live. When enough of these forces stack together, the overall result is a powerful sense that affordability is slipping away.

This is why the phrase “inflation is down” often lands poorly with the public. Even when the rate of increase slows, prices are still elevated. Inflation coming down does not mean prices go back to where they were. It only means they are rising more slowly than before. If the base level has already jumped significantly, especially over several years, households are still living with that higher cost structure. A lower inflation rate may be good news for economists, but it does not automatically feel like relief to families still absorbing the cumulative damage.

Younger professionals and families may feel this even more intensely because the expenses dominating their lives are often the ones most detached from headline inflation. Rent, homeownership, childcare, healthcare, insurance, education, and transportation can all rise faster than the broader averages suggest. If your life stage is concentrated around those categories, your personal inflation rate may feel much higher than the official one. That helps explain why so many people feel as though the economy described in the data is not the same one they are experiencing in daily life.

None of this means inflation data is fake or useless. It means it has limits. It is a broad tool, not a perfect mirror of every household’s reality. Statistics are useful for understanding trends, but they cannot fully capture the emotional and practical burden of declining quality, rising complexity, and the growing effort required just to maintain the same standard of living.

That is the real reason everything feels more expensive than inflation says. The official number is measuring an average. Your life is not an average. It is a specific mix of housing costs, healthcare needs, family obligations, product quality, time constraints, and financial tradeoffs. And if the categories that matter most to you are rising fastest, while the things you care least about are pulling the average down, then the economy will feel harsher than the headline suggests.

In the end, the disconnect is not just about math. It is about trust. People want economic data to reflect what their lives actually feel like. When it does not, frustration grows. Understanding how inflation is measured, and where that measurement can miss the lived experience, does not make life cheaper. But it does explain why so many households feel like they are working harder just to stay in the same place.

All writings are for educational and entertainment purposes only and does not provide investment or financial advice of any kind.