Can You Retire at 60 With $1 Million? The Math Might Surprise You

It’s one of the most common retirement questions and one of the most misunderstood.

If you’ve saved $1 million by age 60, are you ready to retire?

On paper, it sounds like a clear yes. In reality, the answer is far more nuanced and often surprising.

Because retirement isn’t just about how much you have. It’s about how long it needs to last, how much you plan to spend, and how flexible you’re willing to be along the way.

The Starting Point: A $1 Million Portfolio at 60

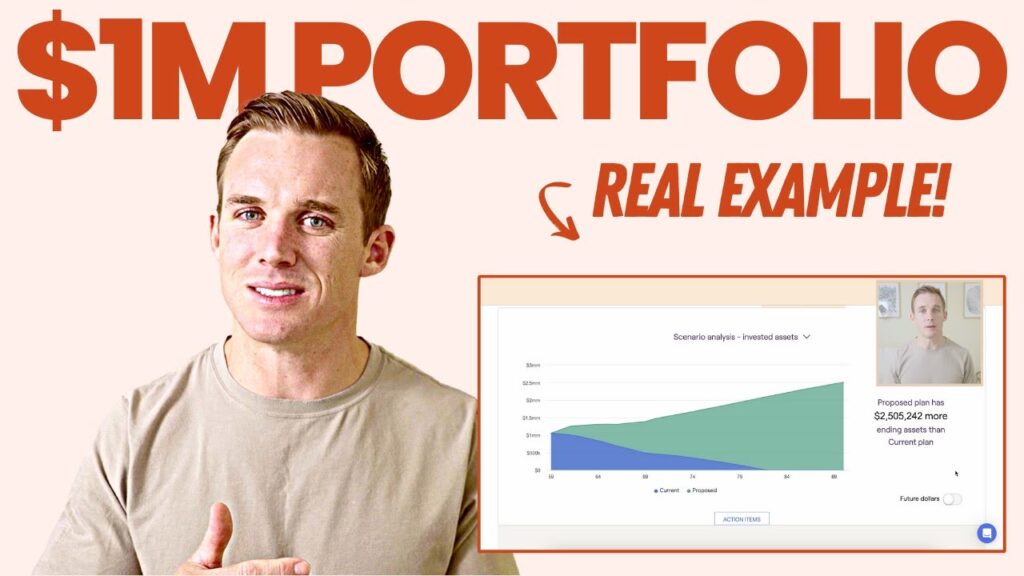

Let’s look at a real-world scenario.

A couple, both age 60, has built a $1 million portfolio across savings, investments, and retirement accounts. Their goal is simple: retire now and live on $8,000 per month, adjusted for inflation.

That’s $96,000 per year in today’s dollars.

At first glance, it feels doable. But when you run the numbers, the challenge becomes clear.

The Problem: An 8.5% Withdrawal Rate

To generate $96,000 annually from a $1 million portfolio, the couple needs to withdraw about 8.5% in the first year.

That’s well above the commonly referenced 4% rule, which is designed to make a portfolio last roughly 30 years.

At 8.5%, the math becomes difficult very quickly.

Even before factoring in inflation, taxes, and market volatility, the portfolio is under significant pressure. Over time, withdrawals increase while the remaining balance shrinks a combination that can lead to depletion in the couple’s late 70s or early 80s.

In other words, the plan works until it doesn’t.

The Social Security Gap

Another key factor is timing.

Social Security doesn’t begin immediately. In this scenario, benefits start later, around age 67 for one spouse and 70 for the other.

That creates a gap.

For several years, the portfolio must carry the full weight of living expenses without support from Social Security. That early strain has a lasting impact on long-term sustainability.

Once benefits begin roughly $5,000 per month combined they help reduce the burden. But by then, the portfolio may already be significantly reduced.

Why Small Changes Make a Huge Difference

Here’s where things get interesting.

Retirement planning isn’t all-or-nothing. Small adjustments can dramatically change the outcome.

For example:

• Delaying retirement by just two years, from 60 to 62, can extend portfolio longevity by more than a decade

• Earning $20,000 per year in part-time income reduces early withdrawals and preserves capital

• Increasing part-time income to $40,000 creates even more breathing room

These aren’t extreme changes. But they have an outsized impact because they reduce the pressure on the portfolio during its most vulnerable years.

Rethinking Expenses: The Retirement Spending Reality

Another assumption worth challenging is how spending behaves over time.

Many plans assume expenses rise at the same rate as inflation every year. But in reality, spending often follows a different pattern sometimes called the “retirement spending smile.”

Spending tends to be higher in early retirement, slows in later years, and may increase again due to healthcare costs.

That means not every dollar needs to grow at a full inflation rate forever.

Adjusting this assumption, even slightly, can make a retirement plan far more sustainable.

It can also create room for discretionary spending, like travel, without jeopardizing long-term stability.

Flexibility Is the Real Strategy

The biggest takeaway isn’t that $1 million is or isn’t enough.

It’s that rigid plans tend to fail, while flexible ones adapt.

Retirement success often comes down to a few key levers:

• When you retire

• How much you spend

• Whether you generate any additional income

• How you adjust based on market conditions

Even modest flexibility working a little longer, spending a little less, or adjusting expectations can dramatically improve outcomes.

The Role of Scenario Planning

This is where tools like Monte Carlo simulations come into play.

Rather than relying on a single projection, they test thousands of potential market scenarios to estimate the probability of success.

A plan with an 85% or higher success rate is generally considered strong.

In many cases, small adjustments are all it takes to move from a risky plan to a resilient one.

The Bottom Line

Retiring at 60 with $1 million is possible but it’s not automatic.

Without adjustments, the math can be tight.

With thoughtful planning, flexibility, and a willingness to make small changes, it becomes much more achievable.

Because in retirement, success isn’t about hitting a single number.

It’s about building a plan that can adapt, evolve, and support the life you actually want to live.

You should always consult a financial, tax, or legal professional familiar about your unique circumstances before making any financial decisions. This material is intended for educational purposes only. Nothing in this material constitutes a solicitation for the sale or purchase of any securities. Any mentioned rates of return are historical or hypothetical in nature and are not a guarantee of future returns.

Past performance does not guarantee future performance. Future returns may be lower or higher. Investments involve risk. Investment values will fluctuate with market conditions, and security positions, when sold, may be worth less or more than their original cost.