How to Actually Reach Financial Freedom: The Strategy That Works

Financial freedom looks different for everyone. For some, it means being debt-free. For others, it’s about living comfortably. But at the end of the day, true financial freedom comes when your passive income covers your lifestyle and you no longer have to work unless you want to.

In this week’s episode, Big Al Klopp and I broke down exactly what it takes to get there and stay there. It’s not just about saving more; it’s about thinking differently about money, time, and the future.

What Financial Freedom Really Means

According to recent data, 54% of people define financial freedom as being debt-free, and 50% say it’s about living comfortably. Only 13% equate it with being rich.

For us, financial freedom means your passive income matches or exceeds your expenses. That’s the point where you get to choose how you spend your time.

But here’s the catch: freedom comes from cash flow, not just net worth. If you have millions in assets but no income from them, you’re still on the clock.

The Roadblocks That Get in the Way

Most people don’t get stuck because they’re lazy. They get stuck because of:

- Not saving enough

- Carrying too much debt

- Living paycheck to paycheck

- Emergencies that wipe out savings

Take credit card debt as an example. The average balance is $8,600, and if you pay just $272 per month, you’ll be at it for 53 months and spend $5,600 in interest.

If you want freedom, the first step is cutting the chains and for many, that starts with credit cards.

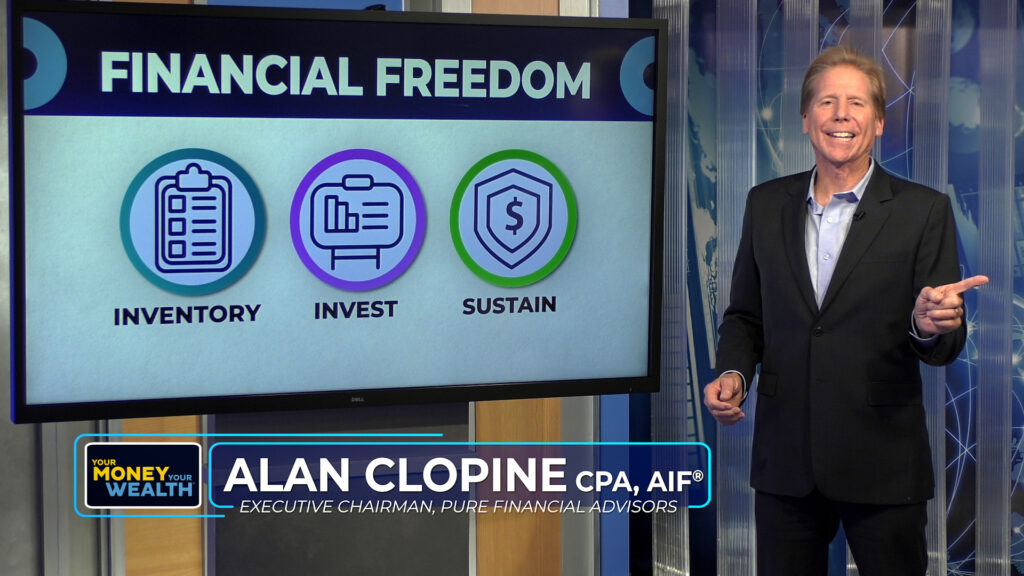

3 Steps to Financial Freedom

Big Al and I recommend this simple process:

- Inventory – Know your numbers: assets, liabilities, net worth

- Invest – Grow your money through smart allocation

- Sustain – Build systems to maintain freedom over time

Calculating your net worth is key. Add up what you own (bank accounts, retirement plans, real estate, etc.) and subtract what you owe (mortgages, loans, credit card balances). That’s your starting point.

And remember: always pay yourself first. Before you spend on wants, contribute to your 401(k), IRA, or savings account.

Taxes: The Sneaky Expense That Eats Your Freedom

Taxes are one of the biggest threats to financial independence. In California, a single filer earning $100,000 nets just $72,000 after taxes.

Want to fight back? Use:

- 401(k) and IRA contributions to lower taxable income

- Roth accounts for tax-free growth

- Capital gains strategies married couples can pay 0% on gains if income is under $94,000

And don’t forget: IRA and 401(k) withdrawals in retirement are taxed like ordinary income. Plan ahead, or risk surprise tax bills later.

Retirement Savings: It’s Never Too Early (But Don’t Wait)

The math is simple. If you start saving $700/month at age 30, you could hit $1 million by 65. Wait until 50, and you’ll need $3,500/month to get there.

That’s the power of compound interest time is your biggest ally.

If you’re self-employed, look into:

- Solo 401(k)s

- SEP IRAs

- SIMPLE plans

And if your employer offers a match? Don’t leave free money on the table.

Build an Emergency Fund (Before You Need It)

Before you start investing aggressively, make sure you’ve got 3–6 months of expenses saved in a high-yield savings account. This keeps you from falling back on high-interest credit cards during emergencies.

Also:

- Set up automatic bill payments

- Monitor your accounts

- Improve your credit score by paying on time and keeping usage low

Passive Income: The Secret Sauce to Sustainable Freedom

Want freedom? You need income streams that don’t depend on you clocking in.

Some options include:

- Rental properties

- REITs

- Dividend-paying stocks

- Social Security

If you wait until age 70 to claim Social Security, you’ll get 124% more than if you claim early. That’s a massive difference.

Plus, don’t underestimate side hustles like freelancing, consulting, or tutoring especially in the early stages of retirement.

Keep Adjusting Because Life Will

Markets change. Taxes change. Health changes. You need a plan that can adapt.

That’s why we talk about the 4% rule a guideline, not gospel. Some years, you may need to pull back to preserve your portfolio. That’s called managing sequence of returns risk retiring into a bad market could force you to sell investments at a loss.

Check in on your plan regularly and pivot when needed. Flexibility is freedom.

Final Thoughts

Financial freedom isn’t about getting rich. It’s about getting clear. Clear on your income, your expenses, your values, and your goals. It’s about using your money to support the life you want—not the other way around.

Whether you’re just getting started or refining your strategy, remember this: it’s possible. You can have a plan that works, a life that feels right, and a future you’re excited about.

You just have to start.

Intended for educational purposes only. Opinions expressed are not intended as investment advice or to predict future performance. Past performance does not guarantee future results. Neither the information presented, nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. Consult your financial professional before making any investment decisions. Opinions expressed are subject to change without notice.

IMPORTANT DISCLOSURES:

• Investment Advisory and Financial Planning Services are offered through Pure Financial Advisors, LLC. A Registered Investment Advisor.

• Pure Financial Advisors, LLC. does not offer tax or legal advice. Consult with a tax advisor or attorney regarding specific situations.

• Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

• Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

• All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy.

• Intended for educational purposes only and are not intended as individualized advice or a guarantee that you will achieve a desired result. Before implementing any strategies discussed you should consult your tax and financial advisors.