Rethinking Retirement: Balancing Financial Security with Enjoying Life

Traditional retirement planning often focuses on maximizing savings and achieving a high probability of success. But is having a 100% success rate in your financial plan always the best approach? I will explore this question and offers alternative strategies for creating a retirement plan that balances financial security with living life to the fullest.

As the founder of Root Financial, I believe a common pitfall in traditional retirement planning—over-optimizing for financial security at the expense of enjoying life. Through the story of Tim and Jennifer, he shows how a personalized approach can transform the retirement experience.

Client Case Study: Tim and Jennifer

Tim (60) and Jennifer (60) sought deeper planning after working with another advisor. Their financial snapshot includes:

- Tim’s 403(b): $190,000

- Jennifer’s 401(k): $505,000

- Roth IRA: $58,000

- Joint accounts and home equity

Their retirement goals include $8,000 per month for basic expenses and $10,000 annually for travel over the next decade.

Income and Savings Projections

- Tim’s annual income: $76,000 (teacher)

- Jennifer’s annual income: $160,000 (director)

- Social Security: $2,500/month (Tim), $3,100/month (Jennifer)

- Tim’s pension: $4,000/month

They currently save 10% of their salaries into retirement accounts, with Jennifer receiving a 3% employer match.

Retirement Projections and Assumptions

Their current investable assets of $915,000 are projected to grow to $1.86 million by age 67, assuming a 6.9% annual return pre-retirement and 6.3% post-retirement. This portfolio will complement their Social Security and pension income to cover their expenses.

Cash Flow and Expense Analysis

Their retirement income sources will provide $9,600 per month, while their living expenses, including taxes, total $169,165 annually. Expenses account for:

- $24,000/year in mortgage payments until 2034

- $10,000/year for travel until 2039

With inflation-adjusted projections, their plan is sustainable.

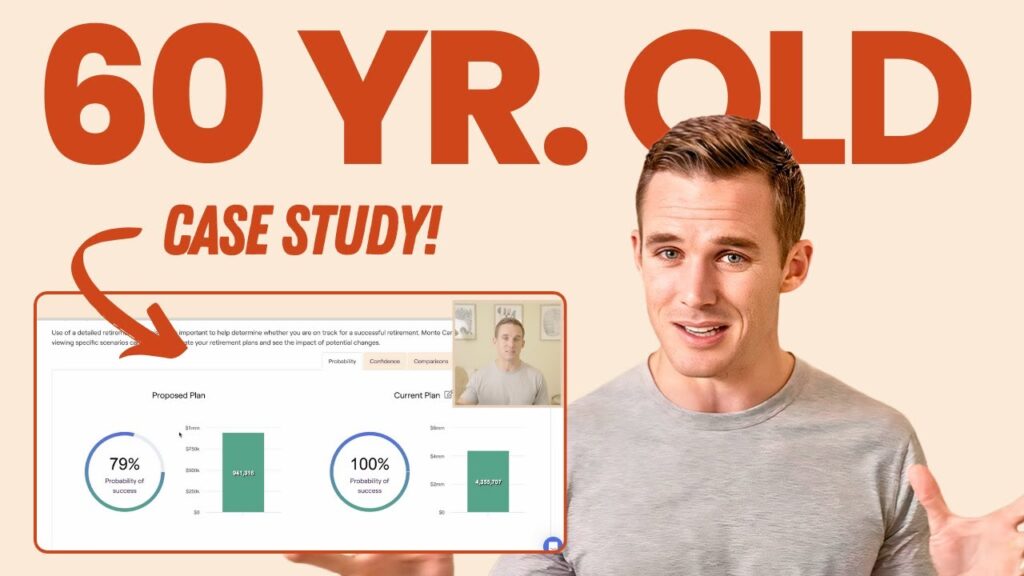

Probability of Success and Risk Management

Monte Carlo analysis shows a 100% success probability, suggesting untapped opportunities. James recommends exploring options such as:

- Retiring earlier (at 62 instead of 67)

- Increasing spending to enjoy retirement years more fully

Adjusting Retirement Plans

While Tim enjoys his job and may work until 65, Jennifer is experiencing burnout and might retire earlier or work part-time. Even with these changes, their financial plan remains robust, maintaining a high probability of success.

The Importance of the Last Five Years Before Retirement

The final five years before retirement are critical for maximizing compound interest and preparing for retirement costs. Examples include:

- Warren Buffett’s wealth doubling after age 56

- The potential for portfolios to double in value during these years

I advise using this period to pay for major expenses, handle medical procedures, and clarify retirement dreams.

Final Takeaways

Retirement planning should go beyond maximizing terminal portfolio value. Instead, focus on optimizing life experiences:

- Consider retiring earlier or adjusting spending habits.

- Balance financial prudence with personal fulfillment.

- Explore options like gifting money to children or charities during your lifetime.

You should always consult a financial, tax, or legal professional familiar about your unique circumstances before making any financial decisions. This material is intended for educational purposes only. Nothing in this material constitutes a solicitation for the sale or purchase of any securities. Any mentioned rates of return are historical or hypothetical in nature and are not a guarantee of future returns.

Past performance does not guarantee future performance. Future returns may be lower or higher. Investments involve risk. Investment values will fluctuate with market conditions, and security positions, when sold, may be worth less or more than their original cost.

A personalized, thoughtful approach to retirement ensures that financial and emotional goals are both achieved. For expert guidance, visit Root Financial to design a plan tailored to your needs.

Related Articles:

- How to Adjust Retirement Plans for Maximum Enjoyment

- The Importance of Balancing Financial and Emotional Retirement Goals

- Monte Carlo Analysis in Retirement Planning