When It Actually Makes Sense to Stop Saving for Retirement

Most retirement advice is built around a single message: save more.

For many households, that is sound counsel. But for a smaller and often quieter group of disciplined savers, the more important question eventually changes. The issue is no longer whether they are saving enough. It is whether continuing to save at the same pace is beginning to crowd out the life they were trying to protect in the first place.

This is one of the least discussed problems in personal finance because it sounds almost too fortunate to take seriously. Yet it is real. A household can spend decades building good habits, maxing out retirement accounts, deferring consumption, and letting compounding do its work, only to arrive in its 50s still acting as if every available dollar must be pushed into the future. By then, the original discipline may still be admirable. It may no longer be necessary.

That is what makes the underlying question so important: when does additional retirement saving stop materially improving retirement security and start mainly increasing the size of an already sufficient estate?

The answer is not emotional. It is mathematical first, then philosophical.

The math matters because compounding changes the balance of the equation over time. Early in a saving life, contributions do most of the heavy lifting. Later, portfolio growth begins to dominate. By the final working years, a large portfolio can grow more from market returns in a single year than many households contribute through active saving. At that point, the portfolio is increasingly financing itself. New contributions still matter, but much less than they once did.

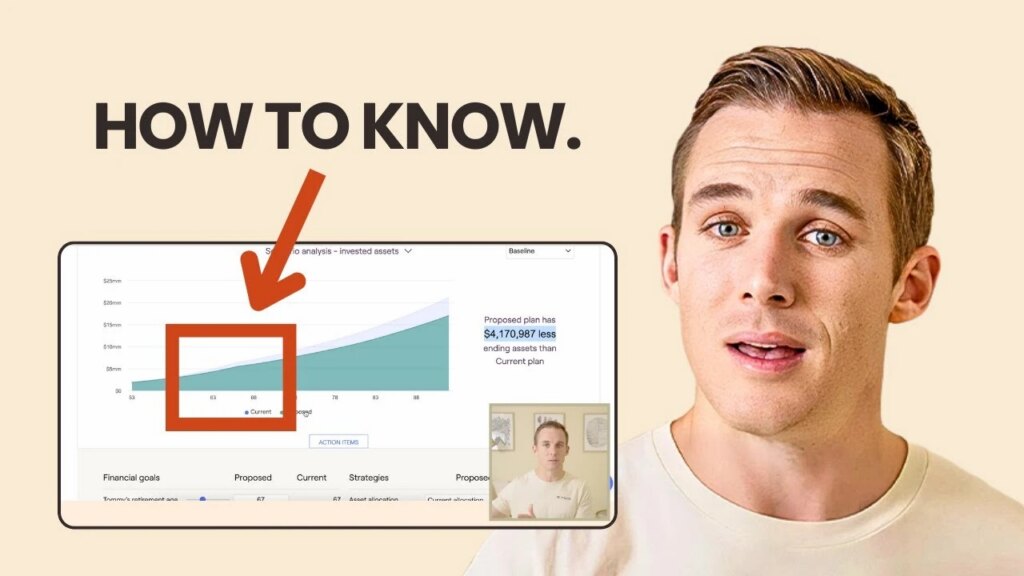

That dynamic is especially clear in the example here. A couple in their early 50s with roughly $2.5 million in net worth, substantial retirement accounts, a brokerage trust account, and strong earnings were saving about 24% of gross income while targeting a retirement lifestyle that was well within the portfolio’s projected capacity. Under reasonable assumptions, the plan already pointed to a retirement portfolio of roughly $6.7 million by the late 60s, with a very low initial withdrawal rate and a projected end-of-life balance that could climb dramatically higher. In other words, the risk was no longer under-saving. It was over-solving a problem that had largely already been solved.

That is where opportunity cost enters the conversation.

Opportunity cost is one of the most important and least appreciated ideas in retirement planning. It does not simply ask what an extra dollar saved today might become in the future. It asks what that dollar is costing in the present if the future is already adequately funded. That cost may not be visible on a statement, but it can be profound in real life. Time with children still at home. Travel while health is good. Family experiences that are age-dependent and cannot simply be recreated later. The point is not to stop being responsible. It is to recognize that there can be a price to endless deferral too.

This is where over-saving becomes a genuine planning issue rather than a rhetorical one. A household may continue contributing at high levels out of habit, identity, or the simple comfort of doing what has always worked. But the continuation of a good habit can still become misaligned if circumstances have changed. A strategy built for scarcity can become unnecessarily rigid once abundance has begun to take over the math.

That does not mean people should abruptly abandon retirement saving the moment projections look strong. It means they should test whether the portfolio still needs the full contribution rate to reach the desired outcome. If modestly reducing contributions still leaves the plan comfortably on track, then the newly available cash flow is not reckless money. It is reclaimed life capacity.

This is what makes the idea so psychologically difficult. Many savers are far more comfortable sacrificing for a future goal than they are spending on the present with intention. The habit of delay can become so ingrained that even when the numbers say “enough,” the person continues acting as though the threat remains immediate. In that sense, over-saving is not really a financial error first. It is a behavioral one. It reflects how hard it can be to switch from accumulation mode to intentional living mode.

The strongest retirement plans are therefore not just projection exercises. They are alignment exercises. They ask not only, “Will you have enough later?” but also, “What are you giving up now that you may not be able to recover later?” This is especially important in the years when children are still at home, when parents are still healthy enough to travel easily, and when work income remains strong enough to support both saving and more deliberate living.

That may mean scaling back Roth IRA contributions, reducing 401(k) deferrals, or simply no longer maxing every available account if doing so no longer changes the retirement outcome in a meaningful way. For the couple in this case, even a sizable reduction in retirement contributions still left the future looking secure, while freeing meaningful annual cash flow for experiences and family priorities in the present. The portfolio at later ages might end up smaller than under the maximum-savings version of the plan, but not meaningfully insufficient. That distinction is everything.

There is also a deeper philosophical point beneath the numbers. Retirement was never supposed to become the sole destination around which the rest of life is starved. Its purpose is to create freedom and security, not to justify the indefinite postponement of enjoyment. If the plan is so future-heavy that it prevents a family from living in ways that matter now, then the financial plan may be succeeding technically while failing personally.

Of course, this advice is not universal. Most people are not in danger of over-saving. Many still need to save more, invest more intelligently, or tighten spending. But for the disciplined minority who have done those things consistently, a different conversation becomes necessary. The question is no longer only how to maximize future wealth. It is how to recognize the point at which additional wealth ceases to be the bottleneck.

That recognition requires confidence, because it means trusting the plan rather than merely repeating the habit. It also requires honesty about what the money is for. If retirement contributions are still being maximized mostly because stopping feels uncomfortable, that is not planning. It is reflex.

The better approach is more intentional. Let the portfolio keep compounding. Continue saving something if it supports the discipline. But if the core retirement goal is already secure, begin redirecting some of the surplus toward the parts of life that cannot be deferred indefinitely.

Because once a plan is strong enough, the most expensive mistake may no longer be saving too little. It may be waiting too long to use the freedom that the saving was meant to create.

You should always consult a financial, tax, or legal professional familiar about your unique circumstances before making any financial decisions. This material is intended for educational purposes only. Nothing in this material constitutes a solicitation for the sale or purchase of any securities. Any mentioned rates of return are historical or hypothetical in nature and are not a guarantee of future returns.

Past performance does not guarantee future performance. Future returns may be lower or higher. Investments involve risk. Investment values will fluctuate with market conditions, and security positions, when sold, may be worth less or more than their original cost.